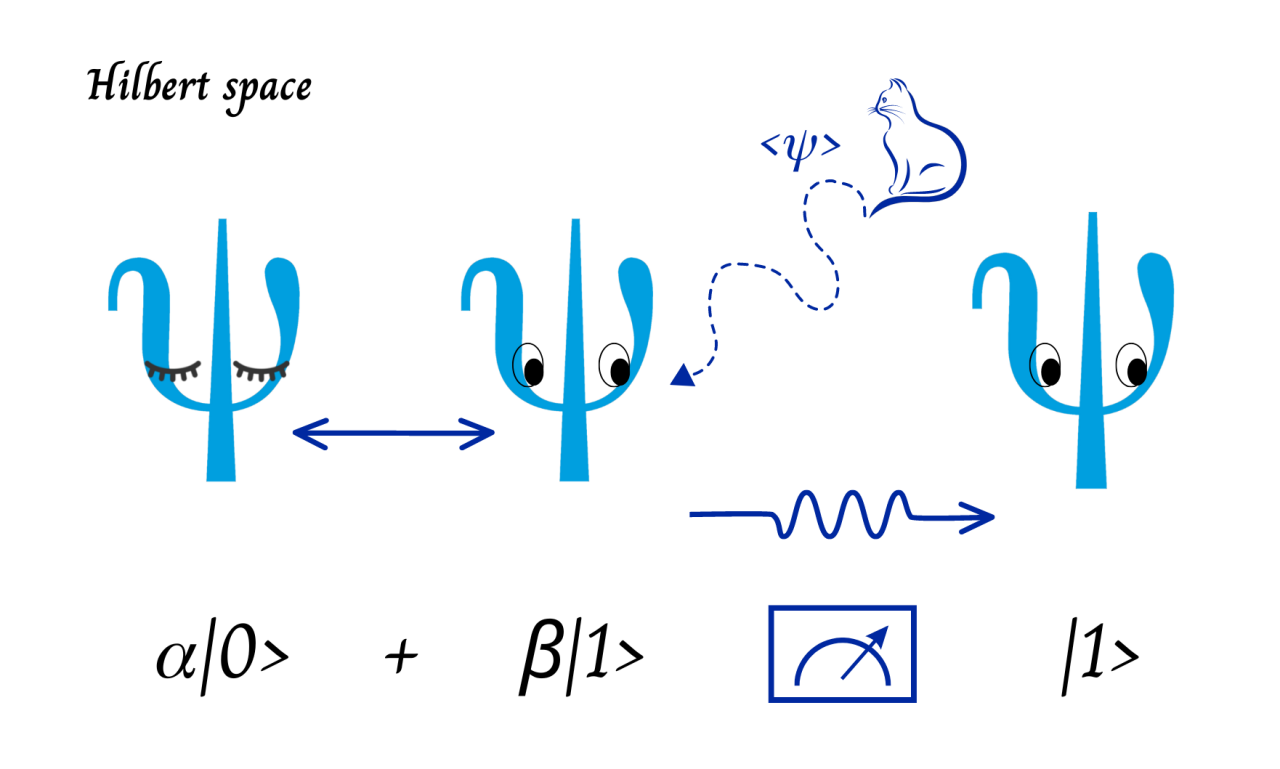

Quantum States, superposition

Perhaps you’ve heard of quantum computing and the seemingly sci-fi nature of how it works. It’s generating interest in many industries with some exciting discoveries and applications. But with all the hype around it, it can be tough to determine what quantum computers can do today. In this article we’ll explore why quantum computing is increasingly relevant to Moody’s.

In 2019, Google claimed to have achieved quantum supremacy when they stated that their Sycamore quantum computer took roughly three minutes to perform a task that would take thousands of years for a supercomputer. This was a fantastic achievement that showed the potential of quantum computing. Even though we are in the early stages of the technology and fault-tolerant quantum computers are still far away in the future, recent work on applications suggests some industries might benefit from quantum computing even in the short term.

The finance industry will probably be one of the first to benefit from quantum computing. Finance has many use cases that require large amounts of live data and complex computational tasks like stock prediction, portfolio optimization, and derivative pricing to name a few. The methods that are used to tackle these problems take a lot of time and space in today’s classical computers. However, some of these can be adapted to quantum computing and will potentially be solved effectively even in near-term quantum devices, providing an advantage vs the classical approach.

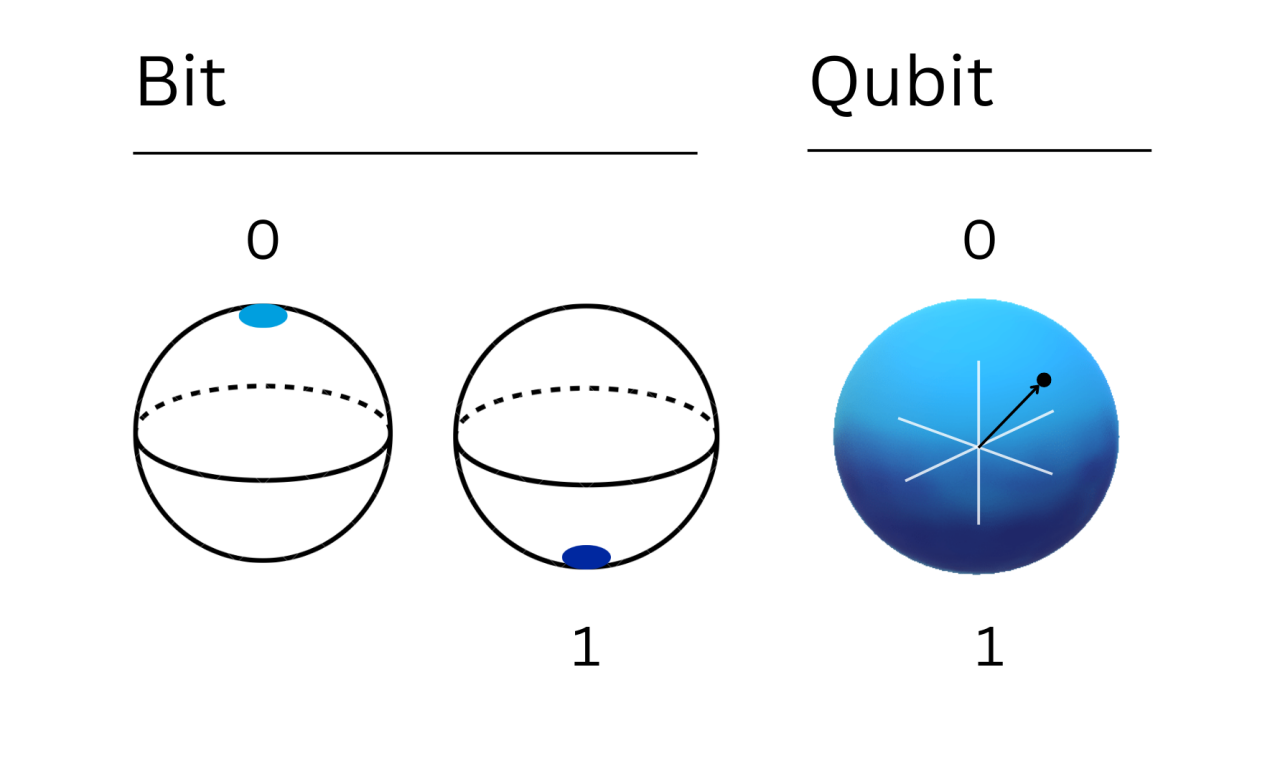

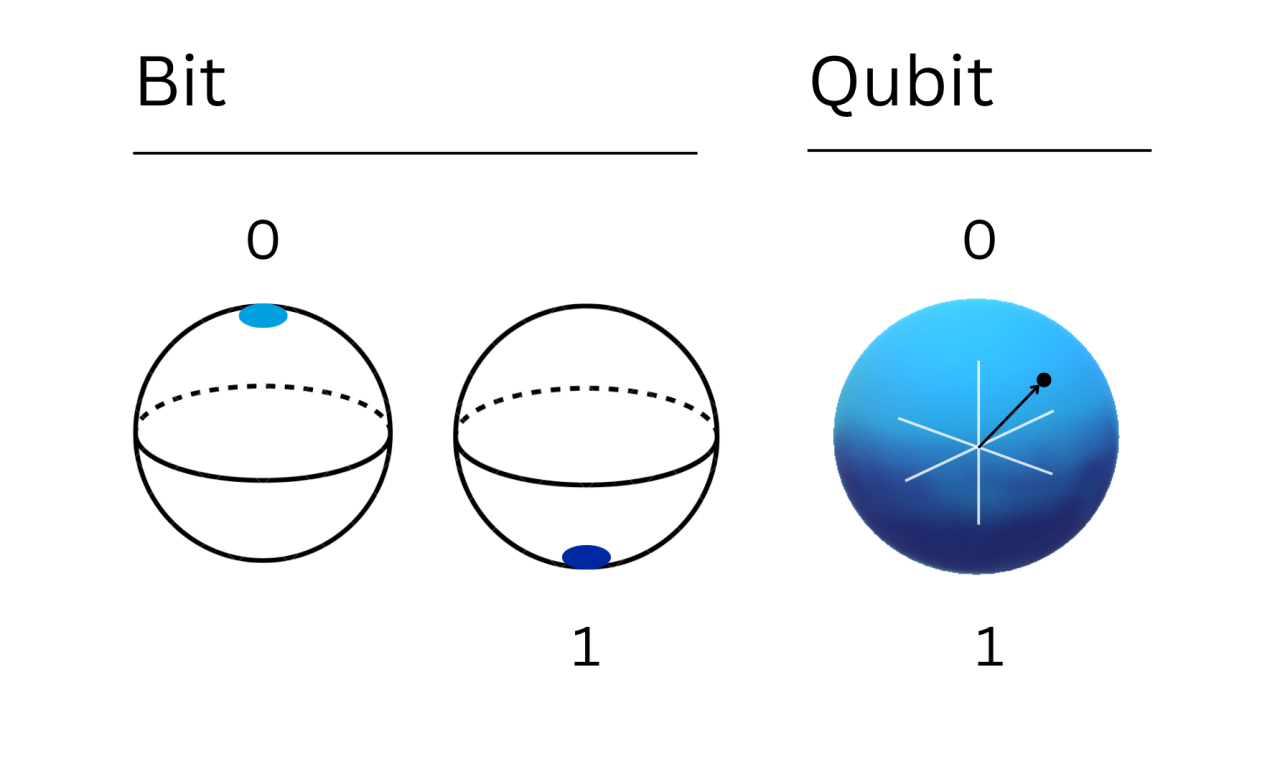

With so many amazing possibilities in the quantum revolution, you might be wondering how quantum computing makes possible to find a more efficient solution to some problems. It’s not magic, although it does feel like. In quantum computing, the basic unit of information is the qubit or quantum bit. Whereas classical bits represent information in the form of ‘0’ or ‘1’, quantum states can be ‘0’, ‘1’ or a combination of ‘0’ and ‘1’. This special property of qubits that allows them to represent information as a mixture of both states is called superposition. Thanks to superposition, N qubits can represent 2N states simultaneously, for that a classical computer would need 2N classical bits. 300 qubits can represent more states than there are atoms in the universe, a “true quantum leap” indeed [2].

Bit vs Qubit

Quantum states are represented as vectors in a so-called “Hilbert Space”. These vectors are denoted by using Dirac’s bra-ket notation |Ψ>. The qubit shown below is in a state of superposition between ‘0’ and ‘1’ (basis states) with some probability amplitude α and β that satisfy |α|2 + |β|2= 1. Now what happens when this state is measured? If you do not measure the state, you are in a bizarre quantum world where you can manipulate the quantum state but when you measure the state, it collapses to one of the basis states, it will collapse to ‘0’ with probability |α|2 or to ‘1’ with probability |β|2.

Quantum States, superposition

Entanglement

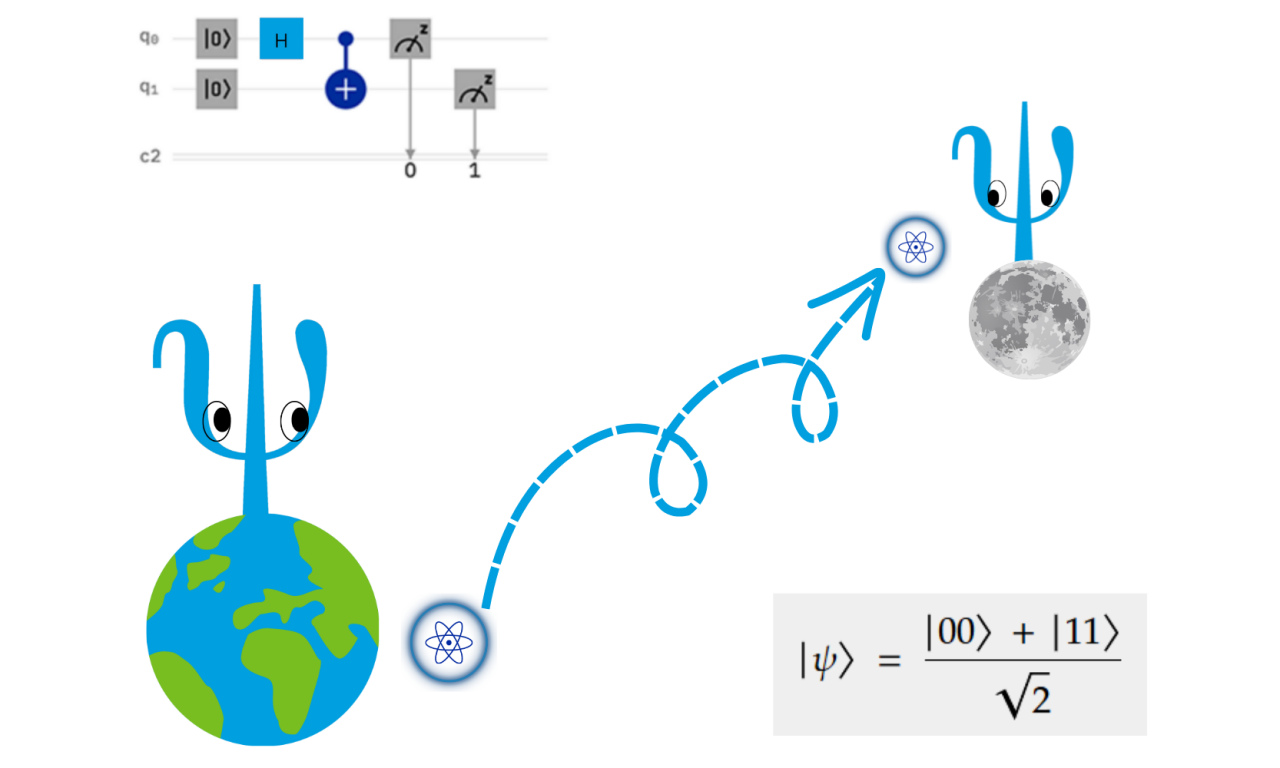

Now that we know what qubit states look like, how do we perform operations on them? Similar to classical bit states, qubit states can be changed by using quantum gates. However, one of the most interesting properties of qubits is ‘entanglement’. A pair of qubits are said to be entangled when the qubits are in such a state that the action on one qubit impacts the state of the other qubit, even if they are far away

from each other. As depicted in the above picture, you can see the quantum entangled state in the bottom right corner and the corresponding circuit [4], that is, the set of gates we need to apply to the qubits to get the resulting state, in the top left corner. Another important property is interference, we can manipulate qubit states in such a way that the states which contain the information we need have their probability amplitudes amplified whereas those that we are not interested in, have their probability amplitudes cancelled out.

Quantum algorithms leverage superposition, entanglement, and interference to solve some problems in a more efficient way.

TOTAL IMPACT OVER

3+ YEARS

TOTAL IMPACT OVER

20+ YEARS

AVERAGE YEARLY BUDGET FROM MOST FORTUNE 500 COMPANIES

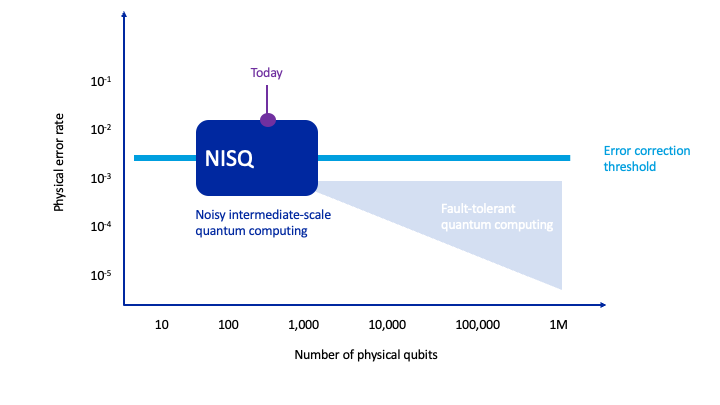

From NISQ to error-corrected quantum computers.

Adapted from Rigetti

Quantum computing is a new paradigm in computing, but there are many open challenges to work on. Creating and maintaining the state of a qubit is not an easy task. Even a small change in the environment can make a qubit unstable, quantum chips based in superconducting qubits, widely used today, are kept in a dilution fridge of almost absolute zero temperature. Some research groups and companies are working on building qubits that can be scaled and maintained at room temperature – including technologies with laser trapped ions or diamonds. Moreover, today’s quantum computers do not have error correction and they contain noise, we refer to them as Noisy Intermediate Scale Quantum (NISQ) quantum computers.

Current quantum algorithms are run in NISQ devices employing error mitigation techniques. The quantum computers that we have today are composed of a few hundred qubits and therefore the size of the problems they can handle is still moderate. But it is not just about the number of qubits. There is more than one metric needed to measure quantum computing performance. According to IBM Research the key three metrics are scale (number of qubits), quality (Quantum Volume) and speed (Circuit Layer Operations Per Second, CLOPS) [3].

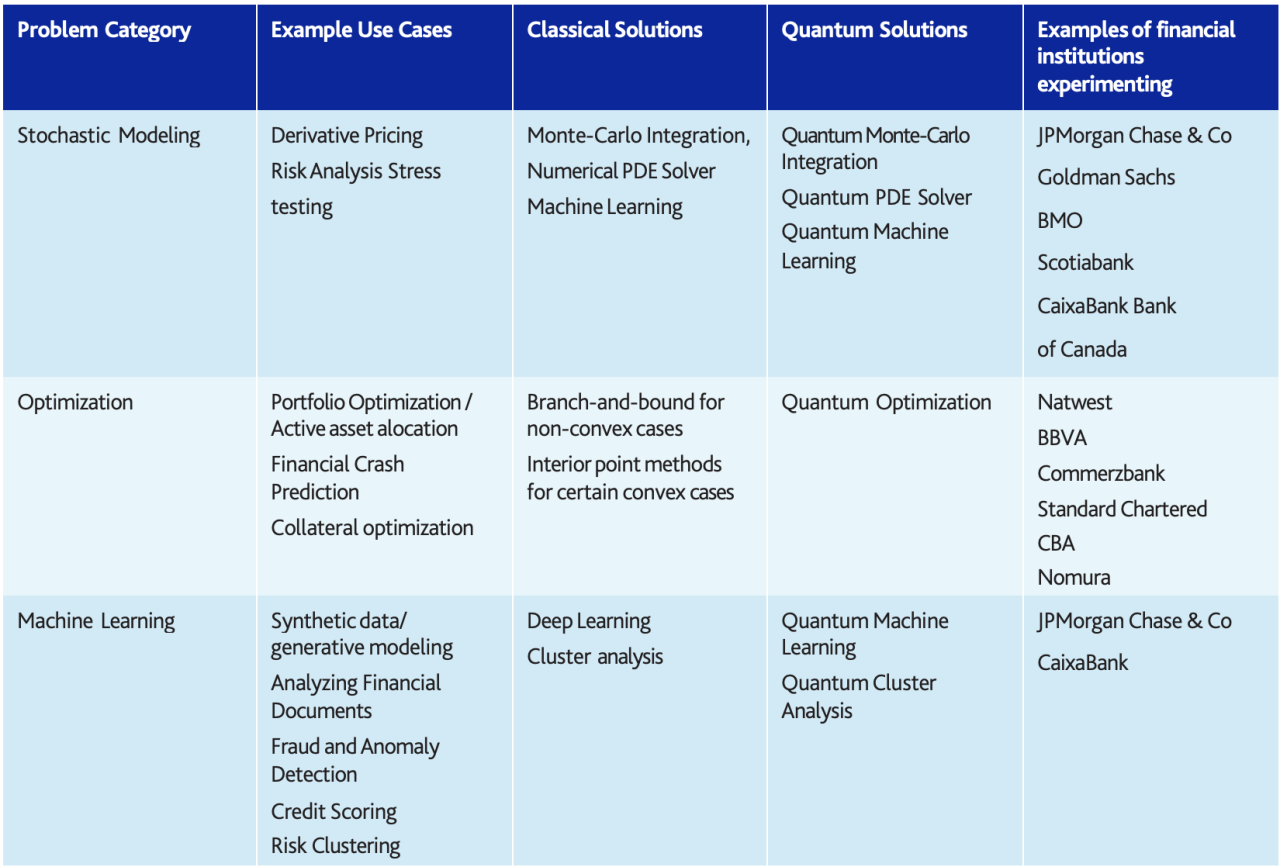

Now the biggest question is, how will quantum disrupt the financial industry? Who will benefit from this and how? Although the power of quantum computing is still beginning to show and there are many open questions, major financial institutions such as JPMorgan Chase & Co, Goldman Sachs, HSBC or Barclays have been working for some years to understand how to harness quantum computing. At Moody’s, we announced this year the creation of our Quantum Computing unit and released a set of Frequently Asked Questions on why we are investing on this.

As mentioned earlier, finance is believed to be one of the first sectors to benefit from quantum computing. Some use cases have the potential to be solved by quantum algorithms designed for near- term quantum computers. Also, when large-scale robust quantum computers become a reality, other quantum algorithms will speed up many computations used in finance. Quantum computing researchers are working on developing quantum algorithms that solve relevant problems more efficiently and building robust quantum hardware. Financial institutions need to understand what benefits quantum computing can bring them:

With improved optimization and decision-making techniques to advance current finance methods and to serve customers better, finance organizations investing in quantum computing at an early stage stand to gain a significant competitive advantage.

Not only will these organizations get a competitive edge, but there are other advantages of being among the first movers too (based on a BCG report).

According to the same report by BCG, it is predicted that quantum computing will create a total impact of $500M in the coming 3+ years and $70B in the coming 20+ years. Right now, the average yearly budget for most Fortune500 companies is $1 million. In 2019, a strategist at Bank of America said quantum computing will be the smartphone of 2020’s and in 2020, a Goldman Sachs researcher pointed out quantum computing as a critical technology [2]. McKinsey also estimates a $3100M industry by 2028 with a 30,8% compound annual growth rate (CAGR).

This is just the tip of the iceberg! At Moody’s, we’re implementing the phenomenal characteristics that quantum physics embeds in computation, and we stand to use that effect to improve current processes in finance. The cases above are some of the examples of cases that will eventually disrupt the financial services industry but surely there will be more.

The road is long but full of discoveries and innovations, and we are here to help you get ready! Join Moody’s in our Quantum Journey by following our group research or participating in our user study groups. Contact us for more information.

References

© 2022 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY’S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS, NON-CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY’S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY’S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDIT RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating, agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000. MCO and Moody’s Investors Service also maintain policies and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody’s Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody’s Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and services rendered by it fees ranging from JPY100,000 to approximately JPY550,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

Visit us at moodysanalytics.com or contact us at a location below:

Americas

+1.212.553.1653

clientservices@moodys.com

EMEA

+44.20.7772.5454

clientservices@moodys.com

Asia-Pacific

+852.3551.3077

clientservices@moodys.com

Japan

+81.3.5408.4100

clientservices@moodys.com