Fifteen of California's twenty most catastrophic wildfires have occurred since 2015.

Over the past decade, major wildfire events coupled with a regulatory environment that has not supported the incorporation of wildfire loss costs based on catastrophe models into rate-making have led some private insurers to pull back from offering coverage in high-risk areas, including not renewing policies.

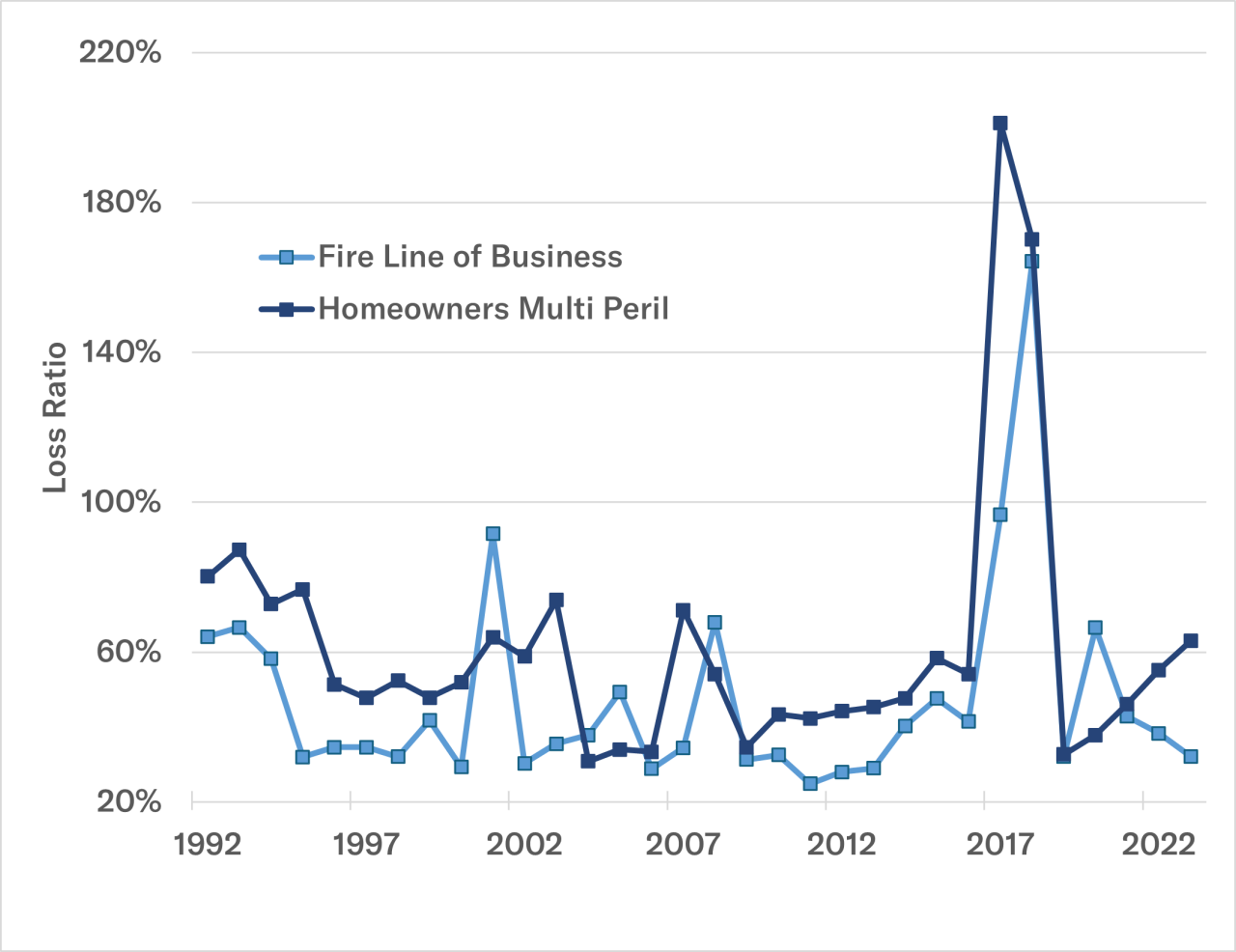

Figure 1: California property and casualty (P&C) historical loss ratios from for fire and homeowners multi-peril lines. Data source: California Department of Insurance. Data includes only California licensed companies with written premium greater than zero.

This trend has left countless homeowners seeking for alternatives, with California’s FAIR Plan intended as a last resort, accumulating high-risk exposure with its portfolio growing from US$50 billion in 2018 to US$458 billion in 2024.

The general perception is that homeowners with non-renewed insurance policies will transition to the FAIR Plan. However, our analysis of recently published data suggests only a fraction of homeowners move to the FAIR Plan, resulting in many finding themselves without coverage or being underinsured.

Not making the transition to the FAIR Plan can happen for various reasons. It could be due to the high costs of FAIR Plan premiums, limited coverage options, simply deciding to self-insure (i.e., have no insurance) if mortgage is paid off, or even not getting around to exploring and deciding on new coverage.

Home insurance is required when having a mortgage on a property, but once the mortgage is paid off, and the lender’s requirement to maintain insurance ends, some homeowners opt out of insurance and may ‘self-insure.’

Without insurance, homeowners are left vulnerable to potentially catastrophic losses after a wildfire. Even when homeowners go for the FAIR Plan, they may opt for limited coverage owing to the high premium.

This current situation in California exposes a significant insurance gap with potentially devastating consequences. Homeowners who choose to self-insure face the daunting prospect of rebuilding their properties without insurance coverage if a disaster occurs.

Additionally, the absence of insurance can hinder community recovery efforts, as uninsured properties may remain damaged or abandoned, affecting the overall resilience and stability of the area.

What does the data suggest in California?

In 2023, the U.S. Senate Budget Committee began a series of hearings examining the risks climate change poses to the insurance, mortgage, and property markets in communities exposed to climate risks.[i]

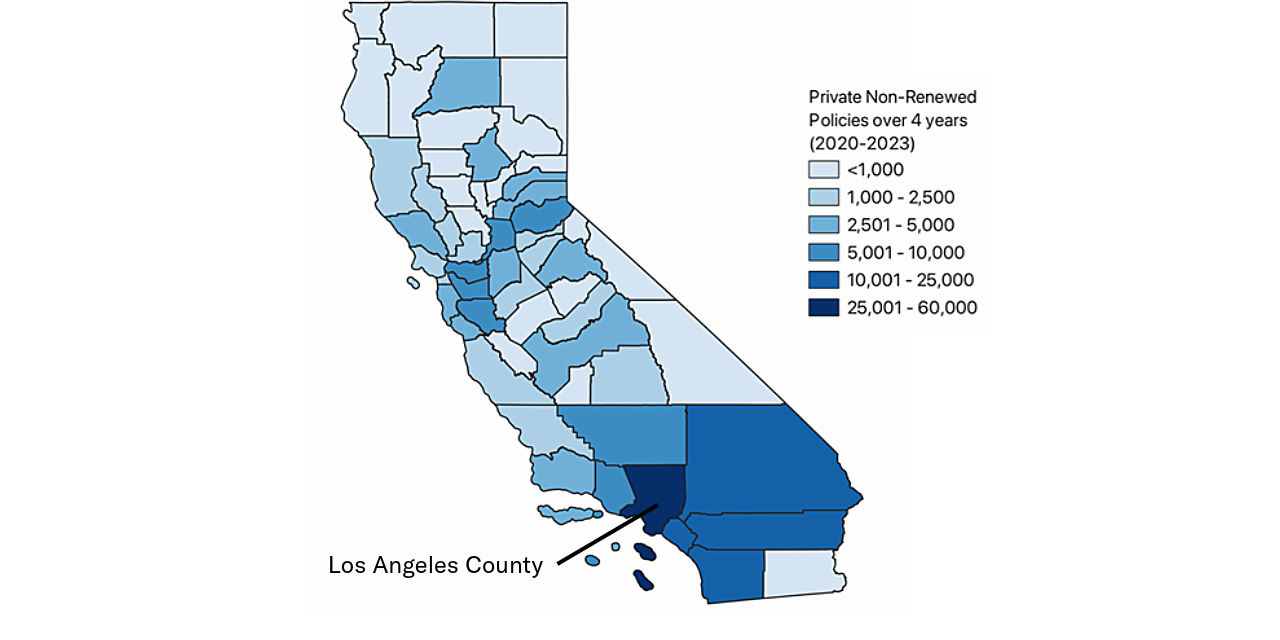

The Committee received substantive data from 23 insurance companies that combined have about a 65 percent share of the U.S. homeowners’ insurance market. The data covers non-renewed residential policies from 2018 through 2023 for all U.S. states. For this blog, we examined the data specific to California from 2020 through to 2023 which corresponds to a total of 257,014 non-renewed residential policies of which 56,558 policies (22 percent) where in Los Angeles County (Figure 2 and Figure 3).

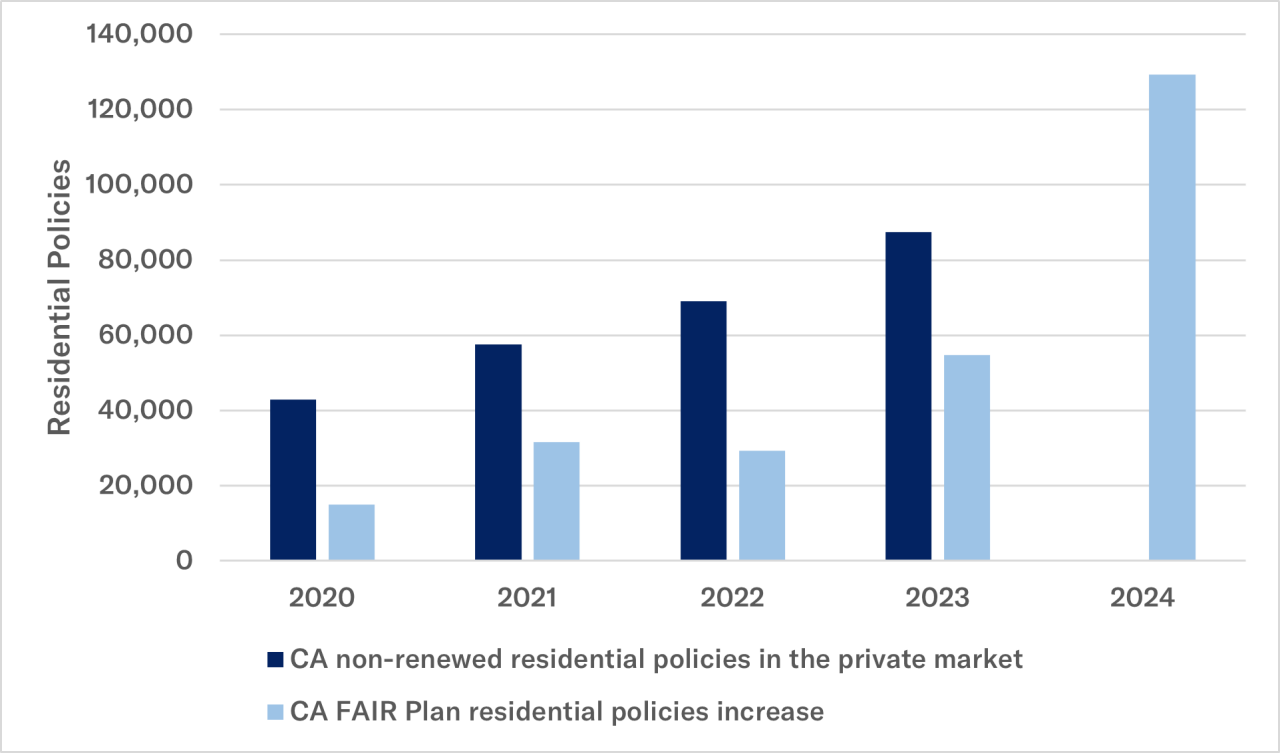

For 2023, the data shows California had 20 percent of overall U.S. non-renewed policies and is the state with the highest number of non-renewed policies in the U.S. When examining the increase in California FAIR Plan policies during 2023, we find a net uptake of 54,663 policies.

If all else is equal, the FAIR Plan uptake compensates for around 60 percent of these non-renewed policies (Figure 3). It is also unclear if these 54,663 policies taken out in California in 2023 meant these homeowners were left underinsured or a proportion of homeowners were able to obtain insurance though surplus lines carriers.

The FAIR Plan while serving as a crucial backstop for homeowners and businesses left without options, also brings to light the challenge of underinsurance. While the market value of homes in the Pacific Palisades area is substantially higher than the state average, a large fraction is the land value. Nevertheless, given the limited coverage available in the FAIR Plan, US$3 million for residential, a significant coverage gap may emerge, potentially leaving many homeowners underinsured against the full scope of disaster-related losses.

Figure 2: County-level non-renewed private policies in California over four years (2020-23). Data source: Staff Report - December 2024 from www.budget.senate.gov.

Figure 3. The number of non-renewed private market insurance policies for California between 2020-23 compared to the net increase in the number of FAIR Plan policies. No data on private policy non-renewals is available yet for 2024. Data sources: Staff Report - December 2024 www.budget.senate.gov and www.cfpnet.com/key-statistics-data.

Los Angeles County

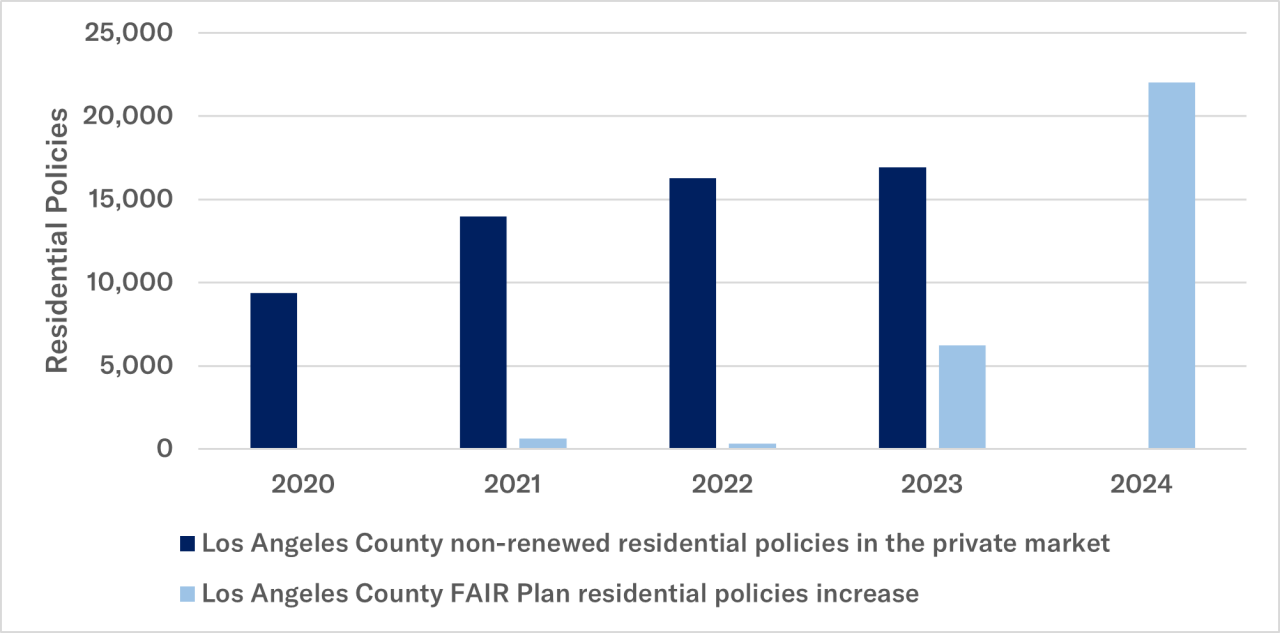

The insurance gap in California varies by County. For example, in Los Angeles County, the proportion of non-renewed policies compared to FAIR Plan policies purchased in 2023 was 37 percent compared to 60 percent across the state, which suggests a larger insurance gap compared to the statewide picture.

The total FAIR Plan policies in Los Angeles County as of September 30, 2024 is 112,945 in (US$112.2 billion exposure) but the growth in number of polices is not keeping pace with the private non-renewed policies (Figure 4).

Los Angeles County exposure represents approximately 23 percent of the entire California FAIR Plan portfolio, and could have been potentially higher at the time of the January 2025 Southernn California fires given the historical trends.

In 2021 and 2022, for example, this figure was a single-digit percentage (see Figure 4 below) suggesting that other private insurance market options were potentially available to homeowners in Los Angeles County.

This discrepancy becomes even more pronounced when considering the average FAIR Plan coverage in Los Angeles County is approximately US$993,430, a figure far removed from the realities of Pacific Palisades' high-stakes real estate market. The volatility caused by non-renewals and the non-uniform growth of the FAIR Plan exposure introduces uncertainties when considering take-up rate assumptions in the Industry Exposure Database.

Figure 4. Los Angeles County non-renewed policies from 2020-23 compared to the growth in FAIR Plan policies. No data on private policies non-renewals is available yet for 2024. Data source: Staff Report December 2024 www.budget.senate.gov and https://www.cfpnet.com/key-statistics-data.

In the ZIP Codes hardest hit by the current Los Angeles County firestorms, the FAIR Plan has seen a remarkable surge in residential policies and total exposure (Table 1).

Location | ZIP Code | FAIR Plan Policies (Sep 2024) and % change since 2023 | Exposure (Sep 2024) and % change since 2023 (rounded) | Average Coverage per policy as of Sep 2024 (total exposure and number of policies) (rounded) |

Pacific Palisades | 90272 | 1,430 (up 85%) | $2.95 billion (up 107%) | $2.1 million |

Malibu | 90265 | 2,366 (up 22.3%) | $4.55 billion (up 23.9%) | $1.92 million |

Topanga | 90290 | 1,915 (down 0.4%) | $2.54 billion (up 6.6%) | $1.32 million |

Altadena | 91001 | 958 (up 28.8%) | $946 million (up 47%) | $0.98 million |

Table 1. FAIR Plan residential exposure in some of the hardest hit ZIP Code by the Southern California wildfires.

This gap – where homeowners are neither privately insured nor under the FAIR Plan, suggests that challenges in the insurance market are unlikely to remain confined to insurance.

Insurance is essential to obtaining a mortgage. As coverage becomes less available, affected properties may potentially not be mortgageable if there is no insurance of last resort or premiums become extremely high. Where homeowners cannot take out mortgages on a growing proportion of properties, the question will be how values could potentially decline.

As traditional insurers recalibrate their exposure to wildfire risk, the reliance on the FAIR Plan underscores the continued need for comprehensive solutions that help address both the affordability and adequacy of insurance and introduce a broader narrative of insurance in wildfire-prone areas of California, one of adaptation and resilience in the face of a growing risk landscape.

A step towards a more resilient wildfire insurance landscape

California’s property and casualty insurance landscape is undergoing transformative change with recent regulatory approval to use catastrophe models to develop loss costs for wildfire rate-making. This development is a key component of the California Department of Insurance (CDI) ‘Sustainable Insurance Strategy’ designed to stabilize California’s insurance market.

On January 2, 2025, changes to California regulations allow for the use of catastrophe models in wildfire ratemaking. The Moody’s RMS U.S. Wildfire HD Model petition to initiate and participate in the Pre-Application Required Information Determination (PRID) certification procedure was granted by the California Department of Insurance.

Moody’s has been actively engaging with the CDI and the insurance market to ensure preparedness and equip insurers with the latest risk assessments to navigate these changes. Regulatory changes by the CDI has established a transparent model review process and will enable carriers to use wildfire catastrophe models to develop loss costs used in rate filings.

The Moody’s RMS wildfire model can bridge the insurance gap by offering a more precise assessment of wildfire risks. The model incorporates mitigation measures, making insurance more accessible in traditionally high-risk areas that have invested in mitigation efforts like vegetation management, structural hardening, and utility undergrounding.

By utilizing advanced modeling techniques, insurers can offer insurance products that accurately reflect the current risk landscape, ensuring more comprehensive coverage and pricing that aligns with the true property risk.

In conclusion, addressing the insurance gap in wildfire-prone areas requires a collaborative effort from different stakeholders including communities, regulators, insurers, and homeowners.

By leveraging advanced modeling techniques and increasing public awareness, we can create a more resilient and equitable insurance landscape that protects all Californians from the growing threat of wildfires.

[i] 'Next to Fall: The Climate-Driven Insurance Crisis is Here – And Getting Worse' - U.S. Senate Budget Committee Staff Report, December 2024.