As Australia’s agricultural sector navigates a dynamic global and domestic landscape, 2025 will be a pivotal year. A recovering domestic economy, shifting global trade dynamics, and easing inflation are opening new growth opportunities – but they’re also exposing producers and lenders to new risks. With two-thirds of Australian agricultural products exported, global pressures like U.S. protectionism and heightened geopolitical tensions weigh on the outlook, while domestic resilience and innovation in agribusiness offer pathways for growth.

In this blog, we explore the economic conditions shaping Australia’s agriculture sector in 2025, the risks and opportunities ahead, and the critical role of lending in supporting the sector’s resilience and productivity.

Domestic conditions: Resilience and recovery

Australia’s economic momentum is building. After seven quarters of per capita contraction, growth turned positive in late 2024, and business and retail activity are picking up. GDP grew 0.6% in the December 2024 quarter and 1.3% year-on-year, and per capita growth was modest at 0.1%, signaling a pickup in economic activity (ABS 2025). Retail sales rose an average of 4.3% year-on-year over the six months to March 2025 (ABS 2025).

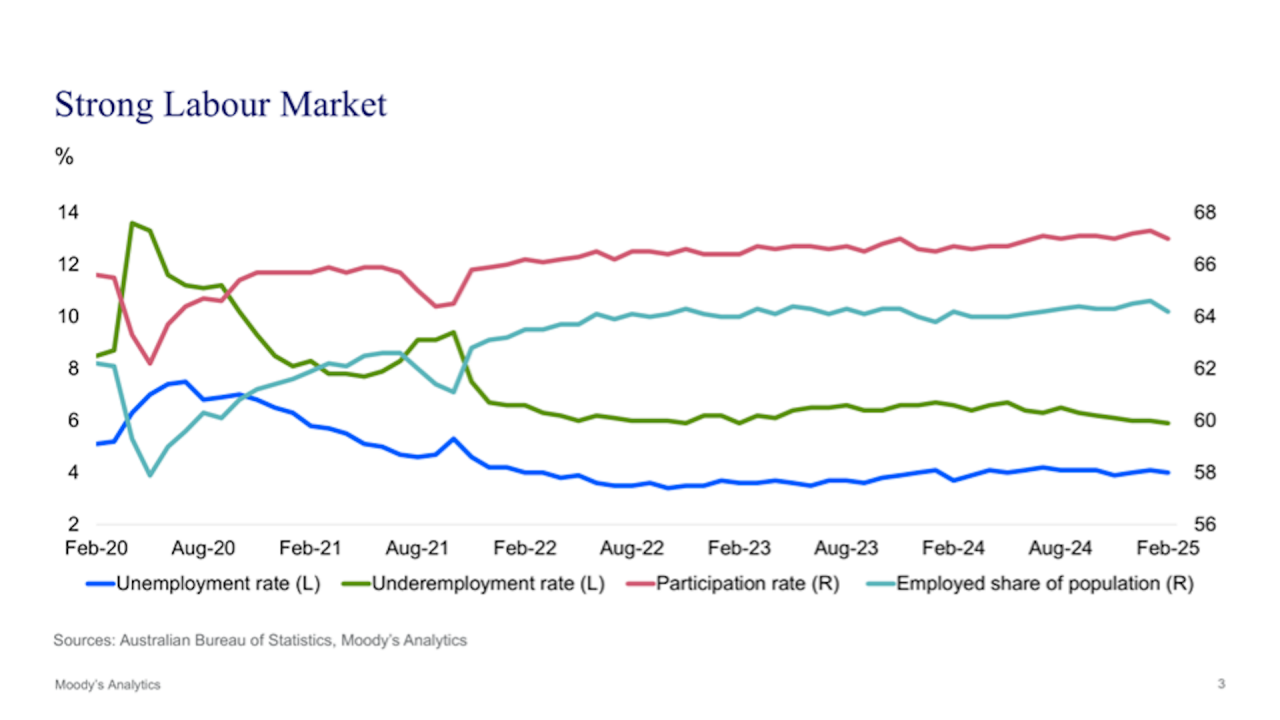

Agriculture is riding the recovery wave, with export turnover for rural goods rising 26% in February compared to the same time last year, largely due to stronger meat shipments (ABS 2025). A strong labor market is also supporting the sector, with record-high participation and employment-to-population ratios are giving farmers access to a steady pool of skilled workers.

Monetary policy: Easing inflation and rate cuts

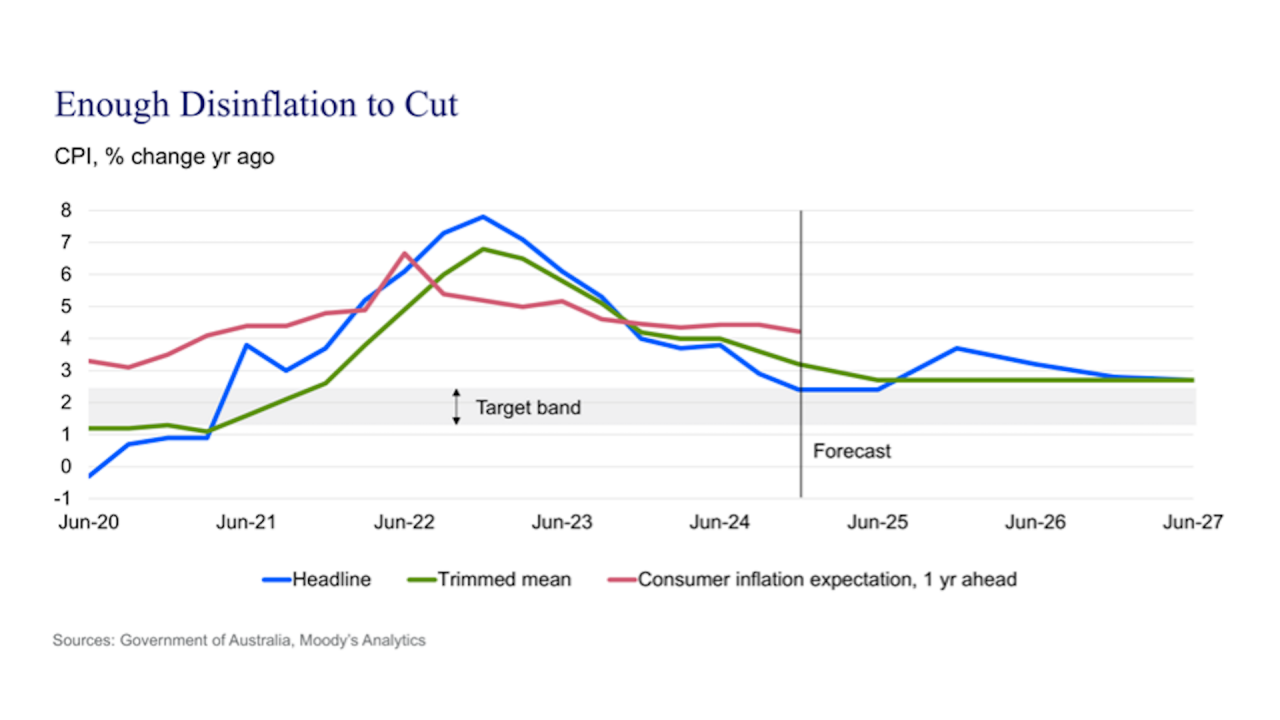

The Reserve Bank of Australia (RBA) began cutting interest rates in early 2025, with inflation expected to average just 2.7% this year. Lower borrowing costs may fuel investment in equipment and technology, while also drawing new entrants into the market, potentially increasing competition and innovation.

However, caution remains – global inflationary risks tied to U.S. protectionism and China’s slowdown could still shape the RBA’s easing pace. Our baseline forecast is that the RBA cuts by a cumulative 75 basis points this year.

External risks: Global trade dynamics and geopolitical tensions

Australia’s agricultural sector is deeply intertwined with global markets, exporting around 70% of its production (ABARES Snapshot 2025). However, global trade dynamics in 2025 present a mixed picture:

- U.S. Tariffs: President Donald Trump’s recent announcements of U.S. tariffs have sparked significant recalibration in global markets. Australian exports to the U.S. will be subject to a 10% tariff, part of the Trump administration's sweeping changes to U.S. trade policy. While not a direct hit to Australia's GDP, they threaten global demand – especially in China – putting pressure on producers reliant on exports. In April, Moody’s downgraded Australia’s 2025 GDP growth forecast to 1.8%, reflecting these challenges. With around 70% of agricultural output bound for export, global tensions remain a key risk. President Trump highlighted Australia's long-standing restrictions on U.S. beef, as U.S. beef imports surge amid reduced domestic supply. Australia has filled the gap, supplying more than 300,000 tons of beef to the U.S. in 2024 – roughly 31% of total beef exports (Meat & Livestock Australia 2025). Any decline in U.S. demand would deal a significant blow to Australian beef producers. Wine exports to the US, Australia's third-largest market, are at their lowest level since the early 2000s, and the situation could worsen with the tariffs in place (Wine Australia 2025).

- Chinese Retaliation: China’s retaliatory tariffs and refusal to renew U.S. meat facility registrations pose a bigger threat to U.S. beef exports, opening doors for other suppliers like Australia. Australian beef -- 31% of which was exported to the U.S. in 2024 -- could pivot to China, where demand remains strong. A weaker Australian dollar would further support producers by softening the impact on beef prices.

- Emerging Opportunities:

- Despite the broader economic uncertainties, new trade dynamics are creating unexpected opportunities for Australia’s agriculture sector—particularly in almonds. Thanks to existing free trade agreements, Australian almond exports to China have surged, growing from just 0.8% of China’s almond imports during Trump’s first term to nearly 70% today (Australian Almond Board 2025). China’s 35% tariffs on Californian almonds have further strengthened Australia's position.

- Likewise, the Australian fruit producers – including apples and stone fruits like cherries— are finding new export openings in markets once dominated by U.S. products, with China remaining their largest export destination. In fact, Australia has achieved a significant milestone by signing a new agreement that will enable mainland-grown apples to be exported to China for the first time in late April 2025 (Apple and Pear Australia 2025). While Tasmania has already been exporting apples to China, this new protocol extends market access to the rest of the country. Following several years of positive dialogue and engagement between the two nations, exports are anticipated to begin in the 2026 season.

- More Australian sheep meat will be exported to China as the country seeks new opportunities amid its trade war with the United States. Ten Australian sheep and goat abattoirs were granted access to the lucrative market, marking the biggest expansion in Australian sheep meat access to China in many years (Australian Meat Industry Council 2025). The new deals provide important competition and relief from the 10% tariffs imposed on Australian exports to the US. China is already the largest buyer of Australian mutton and the second largest buyer of lamb, taking all cuts and weight ranges. The meat industry is optimistic about further Australian red meat opportunities in China, including beef access and potential expansion for other products like tripe.

- Australian canola growers were initially concerned that tariffs on Canadian canola would increase competition in other markets. However, exemptions for certain Canadian products have alleviated these concerns, as the canola will go to the U.S.—a market Australia doesn't trade with. This situation demonstrates the adaptability of Australian agriculture in handling international trade challenges.

Supply chain disruptions and input costs

Despite emerging opportunities, global trade conflicts and geopolitical tensions are disrupting supply chains, potentially causing delays and increasing shipment costs. These costs will raise prices of fertilizer and pesticides in Australia. Meeting administrative requirements around product origin disclosures may slow shipments to the U.S. Middle East conflicts and re-routing are causing volatility in 2025, while global grain supplies could be again threatened if Russia’s war in Ukraine escalates. These higher costs would compress profit margins for producers, particularly those reliant on imported inputs.

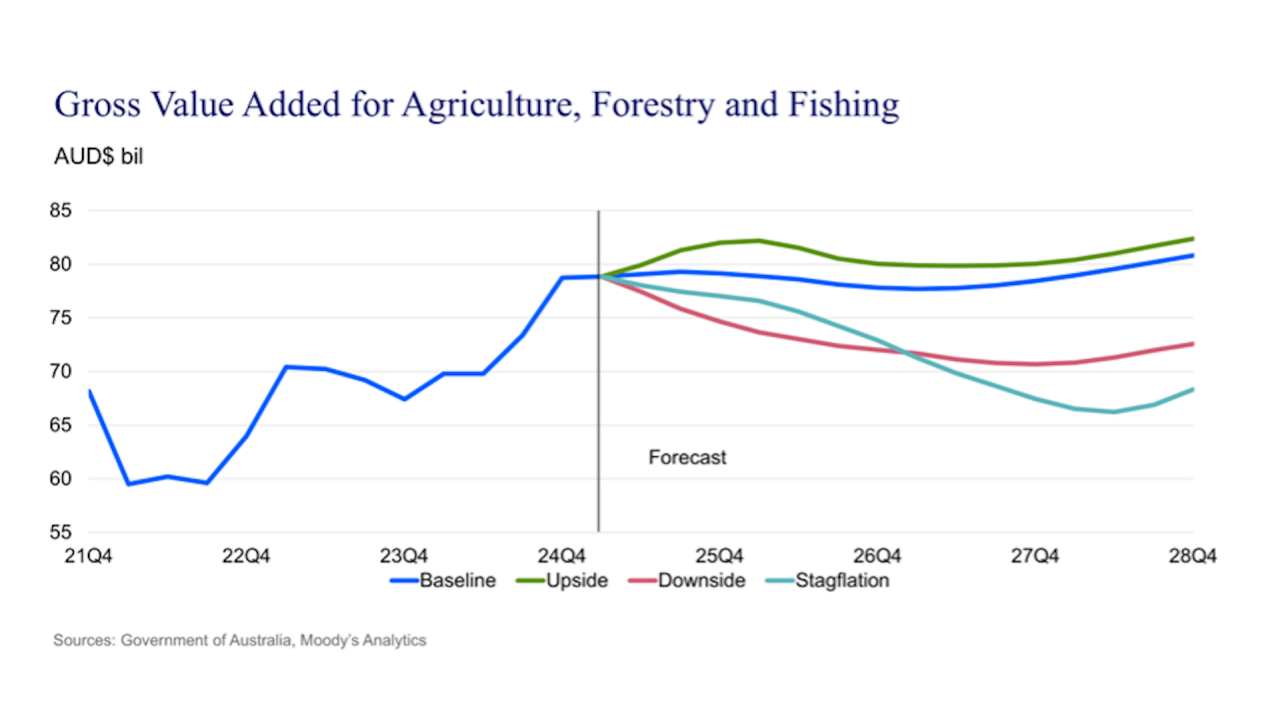

Macroeconomic Scenarios for 2025

Using Moody’s Global Macroeconomic Model, we see four possible paths for Australia’s agriculture sector:

- The baseline scenario is a benchmark against which can be compared with other scenarios.The baseline incorporates the announced U.S. tariffs up to 8th April, including the 10% on Australian exports. We assume that the tariffs quickly ramp up with a peak tariff rate of 17.5% in the second quarter of 2025. Inflation will not spike in this scenario, as retaliation will be muted and there could be some dumping of goods, including autos and clothing, by other countries that find their goods priced out of the U.S. market now. The extension of the electricity rebates will also keep a lid on headline inflation. We expect inflation to stay around 2.5% this year. China's stimulus programs, focusing on infrastructure and property should support demand for key Australian commodities, including agriculture. This steady growth in the sector’s Gross Value Added (GVA) reflects a balance between agricultural productivity and market demand.

- The upside scenario assumes geopolitical conflicts can be resolved much faster than anticipated. The economic policies of the Trump administration have a less detrimental impact on the economy than initially expected. The average U.S. tariff rate on all goods entering the country peaks at 15.5%, compared with 17.5% in the baseline. Tariffs are mostly rolled back by the end of the third quarter of 2025. Better exports and manufacturing output raise business confidence. Wage growth picks up, lifting demand and consumer confidence. The improved global economy, particularly a pickup in China, lifts demand and prices for Australia’s key commodity exports, including agricultural products. The sector's GVA rises 1.8% above the baseline in 2025.

- The downside scenario evaluates the economic policies of the Trump administration affecting the world economy much more negatively than expected. The peak tariff rate is 31.6% and tariffs remain elevated through most of 2028. As global trade collapses, manufacturing and exports nearly come to a standstill. Businesses respond by scaling back investment plans and cutting staff. Consumer and business sentiment goes into free fall. This triggers a deep recession and leads to the agriculture's GVA dropping 3% below the baseline in 2025.

- An alternative potential scenario involves persistent inflation pressure while economic growth takes a hit (this is our Stagflation scenario). This is driven by several factors. The economic policies implemented by the Trump administration have had a more adverse impact on the global economy than initially anticipated. The peak tariff rate is 27.6% and tariffs remain elevated through most of 2027. The geopolitical events, supply-chain disruptions, and a series of economic policy missteps further compound this situation. Energy and food price inflation proves particularly hard to tame. The escalation of supply bottlenecks exacerbates the problem as manufacturers progressively strive to onshore their supply chains.

Greater pass-through from the external shocks to domestic prices adds to this.

- For the agricultural sector, this scenario sees the cost of key inputs such as fuel and fertilizers rise without corresponding increases in output prices, thereby compressing profit margins and reducing GVA. Moreover, economic stagnation may harm consumer demand, compounding the toll on agribusinesses. Although GVA initially declines less (just 1.6% below the baseline) in this scenario than in the downside scenario, the contraction worsens over time and persists for longer. By 2028, GVA is 16% lower than in the baseline.

- For the agricultural sector, this scenario sees the cost of key inputs such as fuel and fertilizers rise without corresponding increases in output prices, thereby compressing profit margins and reducing GVA. Moreover, economic stagnation may harm consumer demand, compounding the toll on agribusinesses. Although GVA initially declines less (just 1.6% below the baseline) in this scenario than in the downside scenario, the contraction worsens over time and persists for longer. By 2028, GVA is 16% lower than in the baseline.

The role of banks: A call to action

While “higher for longer interest rates” are placing some financial strain on the agricultural sector, the level of credit risk across the sector remains stable. Lenders will be critical to this sector’s ability to weather current uncertainty and seize opportunity. The most successful banks will:

- Align loan terms with seasonal cash flow realities of ag operations.

- Use risk analytics to navigate global disruptions and market shifts.

- Monitor and manage risks associated with lending to the sector, particularly those related to physical and transition risk and the transition to a net zero economy.

- Provide producers with timely insights to inform pricing, production, and export strategies.

In short: the more visibility and flexibility banks can provide, the more resilient the sector becomes.

Modernize your agricultural lending process

Learn more

Moody's Lending Suite

Moody's Lending Suite offers a smart, automated solution for effective loan management and confident credit decisions, harnessing advanced analytics and machine learning to deliver a seamless credit experience.