Executive Summary

Our outlook for the global asset management industry in 2025 has moved to stable from negative, reflecting our expectation that lower interest rates and looser monetary policy will accelerate the pace of economic growth globally in the next 12-18 months. Better economic conditions should boost investor confidence and companies' assets under management (AUM).

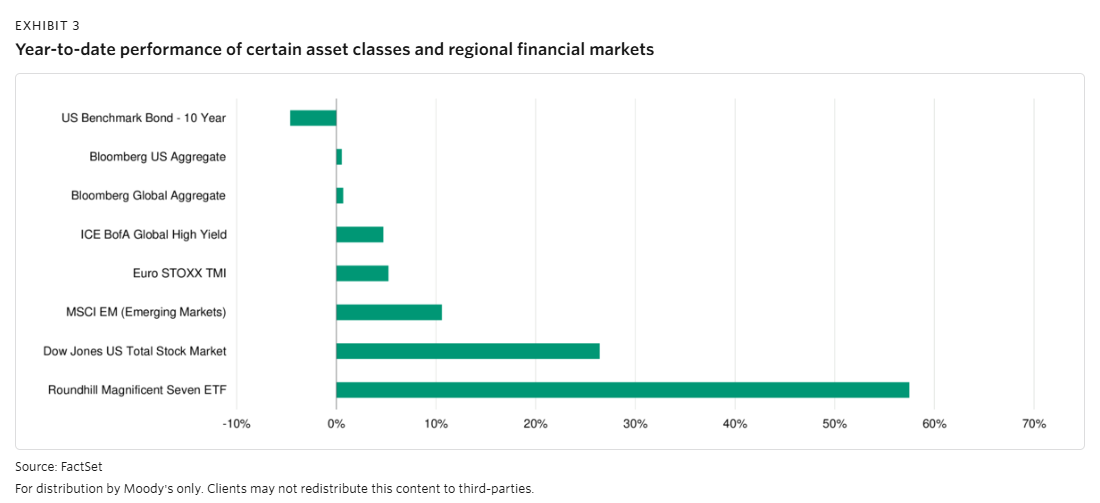

» Continuing global economic growth supports stability in financial market conditions. Equity markets have rallied sharply over the last two years in tandem with sustained global economic growth, particularly in the US. Falling interest rates, facilitated by low and stable inflation, will secure the current expansion. In response to loosening financial conditions and the removal of election uncertainty in many regions, investors will likely re-risk, increasing investment flows and shifting asset allocations to higher-risk asset classes. Increased trade tensions and geopolitical stresses could alter our baseline expectations and trigger a sharp increase in financial market volatility.

» Higher AUM balances will lift industry revenue and margins. Although traditional active managers' operating performance continues to be weakened by rising operating costs and the ongoing shift in industry assets from mutual funds to lower-fee vehicles, such as exchange traded funds (ETFs), the big increase in AUM over the last year will boost revenue and margins heading into 2025. With lower interest rates and positive economic momentum as a backdrop, investors will likely rotate into higher-risk asset classes, a further boost to industry revenue because these asset classes typically yield higher fee rates.

» Industry organic growth should pick up. Although traditional active mutual fund flows as are not likely to turn positive in 2025, rising markets and increased investor confidence will support positive organic growth momentum in other areas such as fixed income, ETFs, SMAs and retail alternatives. Positive economic growth conditions and lower interest rates are conducive to a pickup in private market asset deployments and realizations, which should lead to improvements in private market fundraising.

» Alternative managers will benefit from an improving deal market. In the year ahead, realizations will likely rise alongside lower interest rates, and reduced regulation will likely drive an increase in deal making. Private credit will continue to grow and attract investor flows. A shift in sentiment among legislators could potentially allow alternative asset managers to access the previously inaccessible $11 trillion US 401(k) retirement assets market, significantly expanding their potential investment pool.

ASSET MANAGEMENT OUTLOOK - GLOBAL

View more 2025 outlooks

Learn More

Global sovereigns 2025 outlook

We expect growth and financing conditions to settle in 2025. But geopolitical and social risks and rigid budgets mean governments could struggle to raise living standards.

Global macro 2025 outlook

Monetary policy easing and supportive commodities prices will underpin G-20 economies amid the potential growth-inhibiting effects of rising trade protectionism and festering geopolitical conflict.