Infographic

Commercial real estate conditions will improve, even for office (published 13 Jan 2025)

Commercial real estate conditions will improve, even for office (published 13 Jan 2025)

Executive Summary

As US and European economies grow in 2025, broad-based support for consumer spending will benefit commercial real estate (CRE) revenue. Among new commercial mortgage-backed securities (CMBS) and CRE collateralized loan obligations (CLOs), property sales and issuance will rise and leverage will expand, driven by declining or stable interest rates. For existing transactions, refinancing rates will improve, though maturity defaults will remain elevated for office properties.

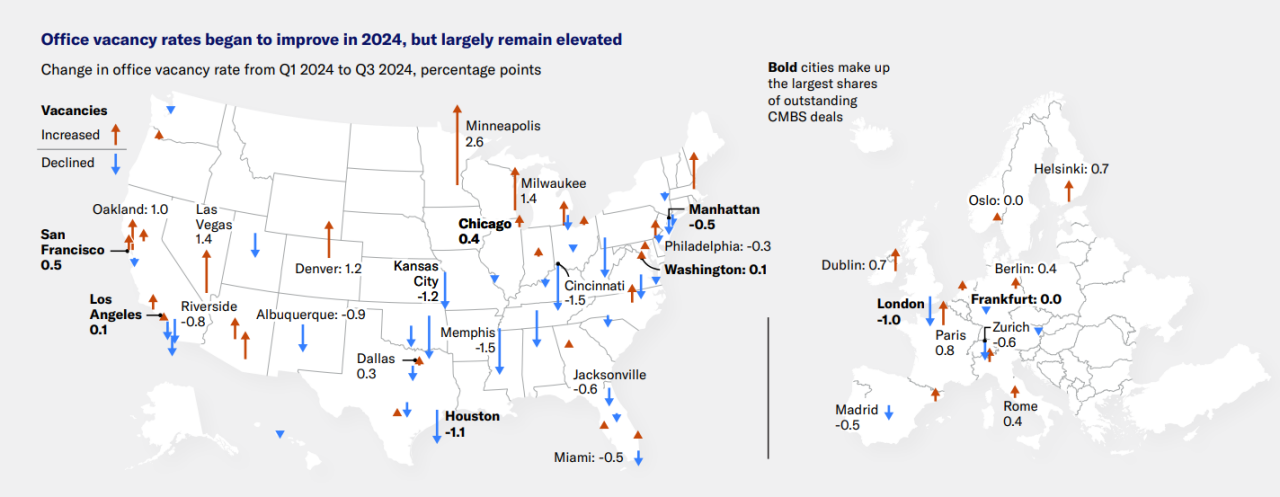

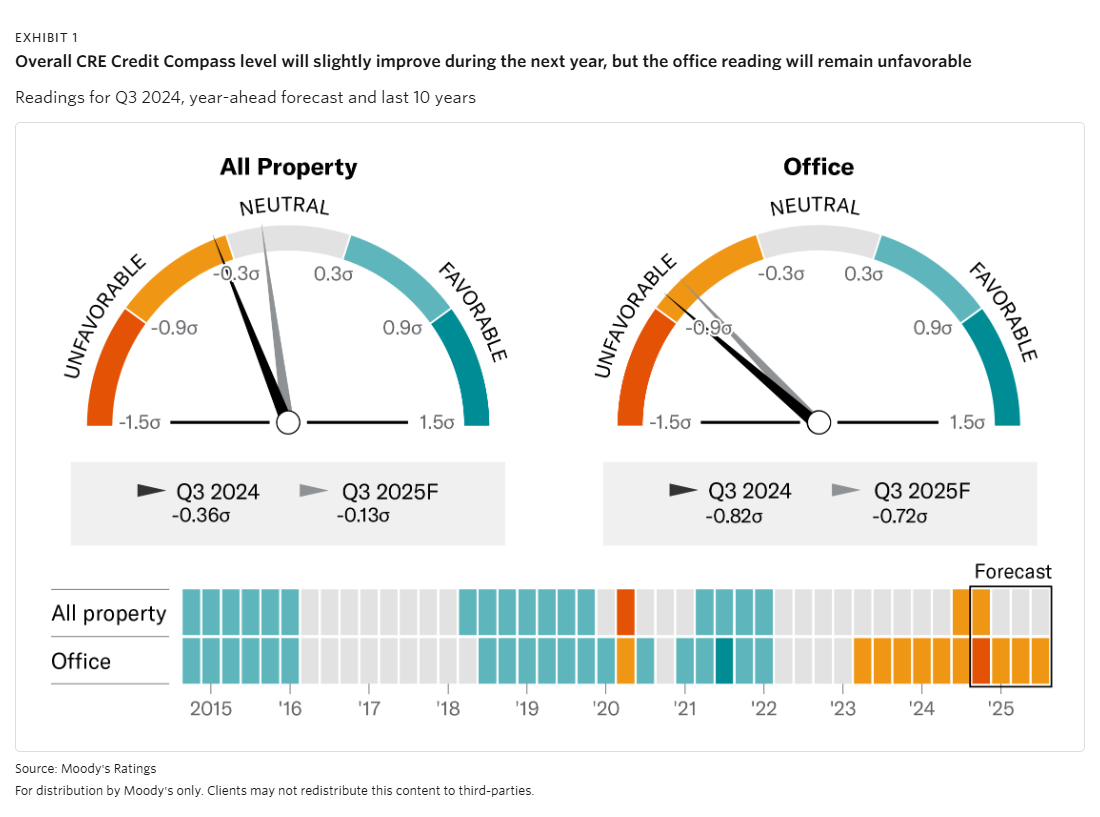

» Property fundamentals: Revenue will expand for most property types; valuations will firm. CRE conditions will improve next year in the US and Europe as macroeconomic factors remain supportive and demand exceeds supply in several property sectors. However, in many office markets, revenues will decrease as leases continue to reset lower, reflecting high vacancy levels and the prevalence of hybrid work. Steady long-term rates will help stabilize property valuations.

» New transactions: Issuance will rise, as will leverage. As floating rates decline and long-term rates stabilize, acquisitions and leverage will increase, financed by large loan (LL) and single asset/single borrower (SASB) transactions and CRE CLOs, leading credit enhancement to expand. Similarly for US conduit transactions, recent rate trends should lead sales transactions and loan-to-value (LTV) ratios to rise.

» Existing transactions: Refinance rates will likely improve, but delinquency rates will remain elevated. Stable-to-lower rates and ample liquidity will increase refinancing opportunities but only for some properties. For example, elevated vacancies will continue to keep office loan refinancing rates low and increase delinquency rates. In Europe, borrowers' high equity levels will help uphold performance. Falling costs to cap interest rates will support US CRE CLO performance.

CMBS and CRE CLOs - GLOBAL

View more 2025 outlooks

Learn More

Global credit conditions 2025 outlook

Steady economic growth and lower interest rates will benefit cash flows and credit, but military conflicts, US policy changes, carbon transition and new technologies will cause disruptions.

Global macro 2025 outlook

Monetary policy easing and supportive commodities prices will underpin G-20 economies amid the potential growth-inhibiting effects of rising trade protectionism and festering geopolitical conflict.