Executive Summary

Structured finance transactions we rate will largely benefit from continued economic growth and declining interest rates in much of the world in 2025.

The continued growth and easing interest rates will support consumer asset-backed securities (ABS) and residential mortgage-backed securities (RMBS), although some consumers' financials remain strained from high costs in recent years. Corporate obligors will also benefit; having reaching cyclical peaks earlier this year, US and European collateralized loan obligation (CLO) collateral defaults will decline in 2025, with support from this past year's strong loan refinancing activity. Macroeconomic factors will also broadly support commercial real estate (CRE) values and borrowers' ability to service debt, though office property and loan performance will remain at heightened risk, reflecting still-high market vacancies and weak rents. Private capital sponsorship of structured finance transactions will continue to grow.

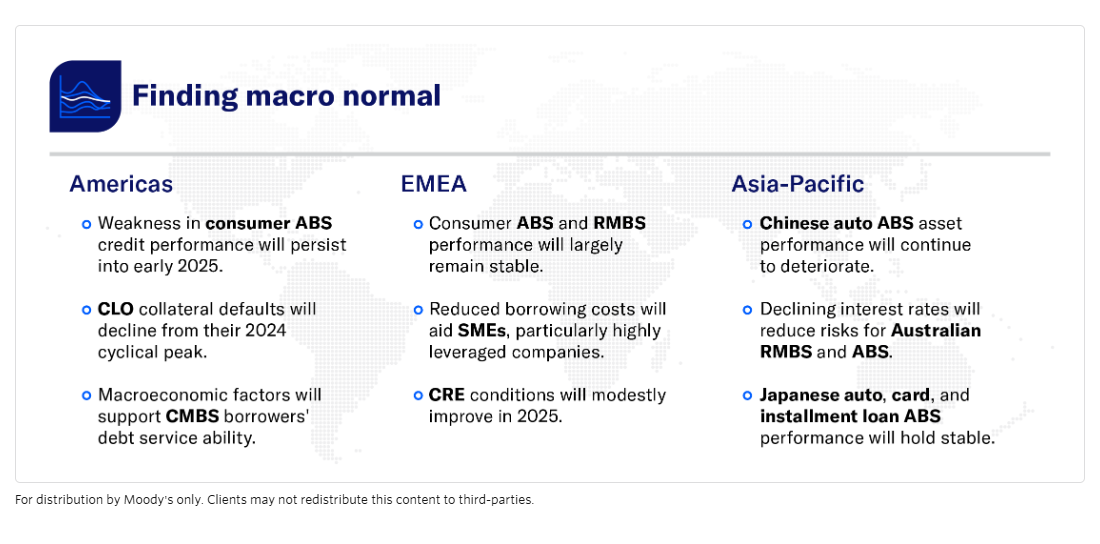

» Finding macro normal: Although global growth is starting to normalize, weakness in US consumer credit performance will persist into early 2025, but stabilize by late in the year. In Europe, easing inflation and declining interest rates lead a shift from negative to stable in our collateral forecasts for UK prime RMBS, Spanish auto ABS, and Spanish and Italian small and medium-sized enterprise (SME) ABS. In Japan, asset performance will hold stable, and declining interest rates will mitigate risks for Australian RMBS and ABS. Asset performance will continue to weaken for the Chinese auto ABS we rate as the country's economic slowdown weighs on incomes, job security and household wealth.

» Geopolitical tensions: Geopolitical tensions pose risk to aircraft ABS, though strong demand will likely offset much of this risk. A continued decline in US net farm income would weaken agriculture equipment ABS obligors' ability to make contract payments, if the incoming presidential administration makes certain changes to trade and immigration policies that raise labor costs and prompt retaliatory tariffs from trade partners.

» Digitalization and disruption: Increasing demand for high density fiber connectivity will continue to uphold digital infrastructure and dark fiber ABS cash flows. With competition between private credit and the broadly syndicated loan (BSL) market intensifying, middle market CLOs will continue to account for a large share of new US CLO issuance.

» Global transitions: Efforts to mitigate climate change will continue to drive increased electric vehicle exposure in Chinese auto ABS, while US exposures remain generally in line with the broader market. However, battery electric vehicle (BEV) penetration in Europe will slow in 2025 despite the launch of new models with technological advancements, enhanced product availability, and continued price adjustments.

You can find a list of all structured finance outlooks for 2025 within the report below.

STRUCTURED FINANCE OUTLOOK - GLOBAL

View more 2025 outlooks

Learn More

Global sovereigns 2025 outlook

We expect growth and financing conditions to settle in 2025. But geopolitical and social risks and rigid budgets mean governments could struggle to raise living standards.

Global macro 2025 outlook

Monetary policy easing and supportive commodities prices will underpin G-20 economies amid the potential growth-inhibiting effects of rising trade protectionism and festering geopolitical conflict.