Executive Summary

Across these diverse landscapes, the interplay of economic policies, consumer behavior, and geopolitical dynamics shapes a cautiously stable outlook for corporations in 2025. Dive into the five regional corporate outlooks for key issues and nuances specific to that region: North America, EMEA, LatAm and Carribean, APAC (ex China), China

» North America - Stable as inflation wanes but stressed consumers, geopolitics add risk

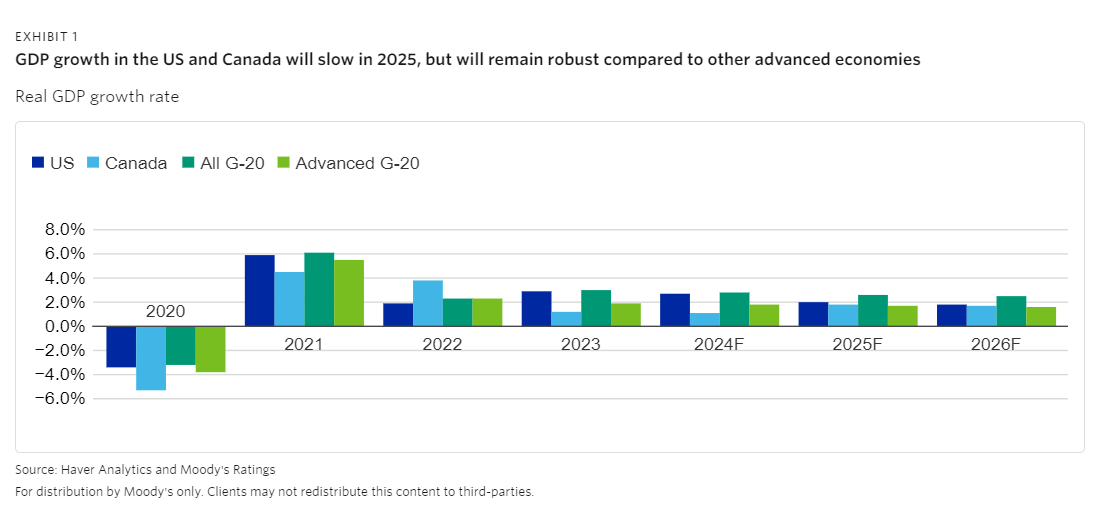

Modest but steady corporate profits, waning inflation and purposeful consumer spending will drive stable credit conditions in most industries. Softening labor demand and still high, if falling, interest rates will pressure credit quality and liquidity and weigh on consumer buying decisions. Real GDP growth in the US (Aaa negative) will remain relatively robust compared with other advanced economies, but the familiar list of geopolitical flashpoints, including US-China trade tensions, the war in Ukraine and conflict in the Middle East, keeps the mood cautious.

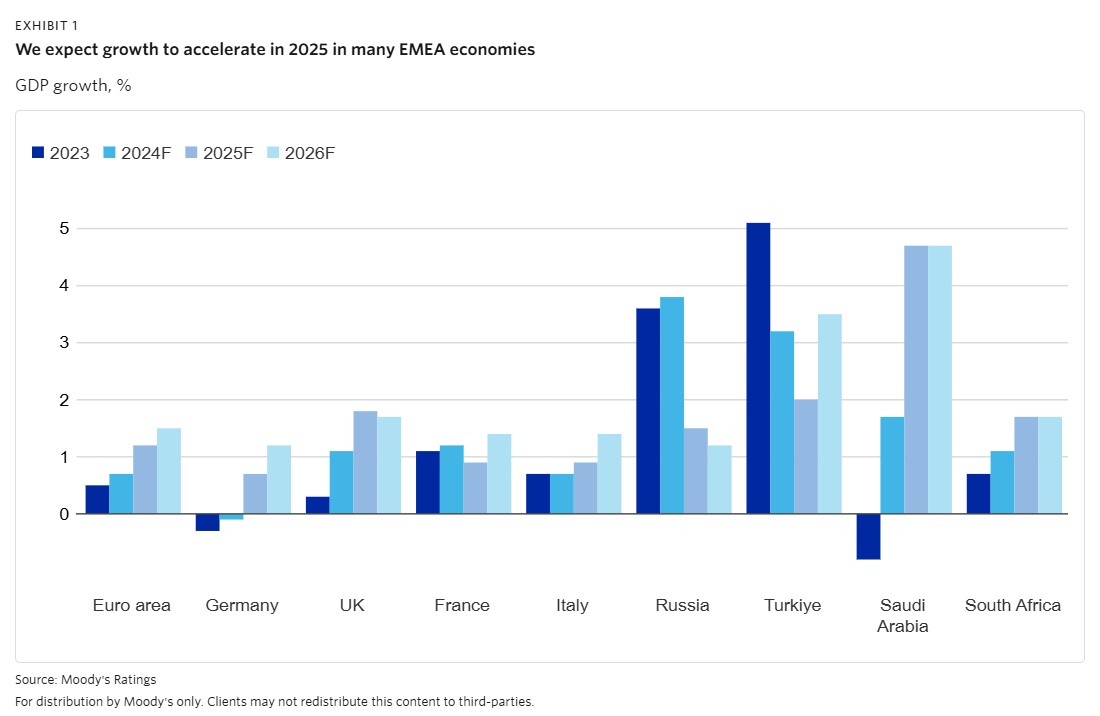

» Europe, the Middle East and Africa (EMEA) - Stable on lower rates, moderate growth, but geopolitics weigh

This is a change from our 2024 outlook, which was negative. Receding inflation, easing monetary policy and a moderate pickup in growth set the stage for slightly improved credit conditions in 2025. But geopolitical risks, uncertainty about trade policy from the incoming Trump administration in the US, structurally high energy costs and cautious consumer sentiment continue to weigh on prospects.

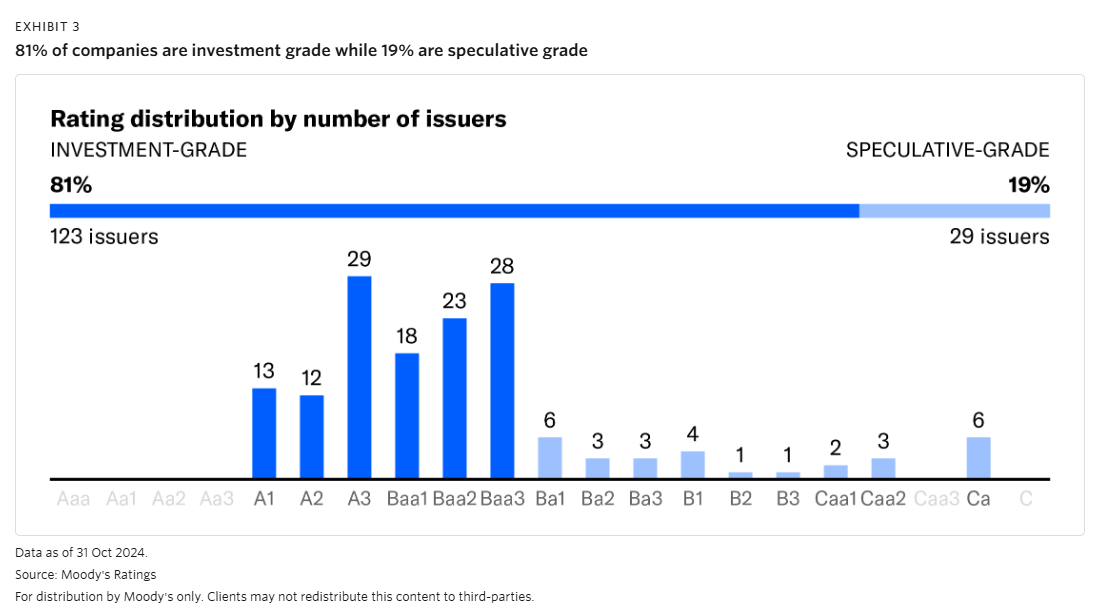

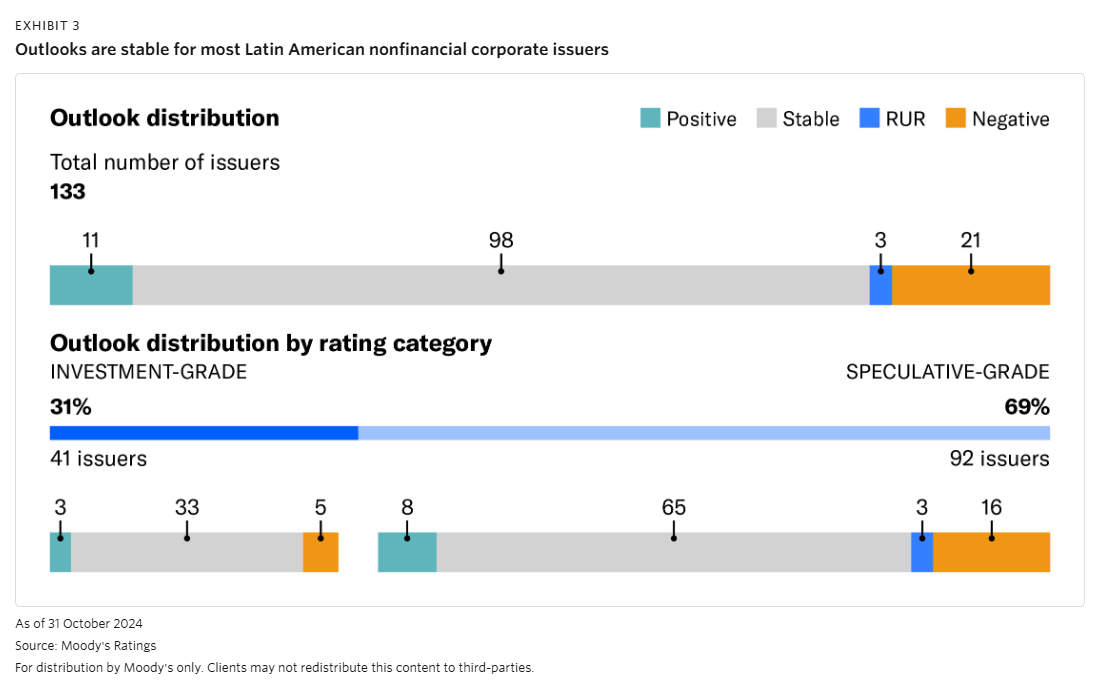

» Latin America & Caribbean - Stable on mixed growth, but operating environment implies hazards

Our stable outlook for 2025 for Latin American nonfinancial companies reflects the region's variable credit implications from four key credit themes that will influence corporate credit quality worldwide: Finding macro normal; geopolitical tensions; global transitions; and digitalization and disruption.

» Asia-Pacific (APAC) excluding China - Stable on growth, easing interest rates, despite geopolitical tensions

The outlook for companies in Asia-Pacific excluding China (APAC) for 2025 is stable. Solid GDP growth, driven by India (Baa3 stable) and Indonesia (Baa2 stable), underpins the region's corporate earnings growth, with nuances across sectors. Easing interest rates will support refinancing and financing conditions. Technological advancements, especially in artificial intelligence (AI), will disrupt traditional sectors, prompting substantial investments. Certain sectors will reap the benefits of diversifying supply chains driven by geopolitical tensions.

» China - Stable amid stronger stimulus, but geopolitical risk has climbed

Our outlook for nonfinancial companies in China for 2025 is stable. This is a change from our outlook for 2023-24, which was negative. While economic growth will likely decelerate , stronger stimulus from the government will prevent credit conditions for nonfinancial companies from further deterioration. Prudent financial policies, narrowing declines in property sales and continued advancement in new growth sectors will also support corporate performance. But elevated geopolitical tensions remain a key risk. We project the aggregate EBITDA of Chinese nonfinancial companies to stabilize in 2025, versus annual declines in 2023-24.