Executive Summary

The global economy has shown remarkable resilience in bouncing back from supply chain disruptions during a pandemic, an energy and food crisis as the Russia-Ukraine war began, high inflation and consequent monetary policy tightening. Most G-20 economies will experience steady growth and continue to benefit from policy easing and supportive commodity prices.

However, postelection changes in US (Aaa negative) domestic and international policies could impact macro conditions and potentially accelerate global economic fragmentation, complicating ongoing stabilization. The aggregate and net effects of trade, fiscal, immigration and regulatory policy changes will expand the range of outcomes for countries and sectors.

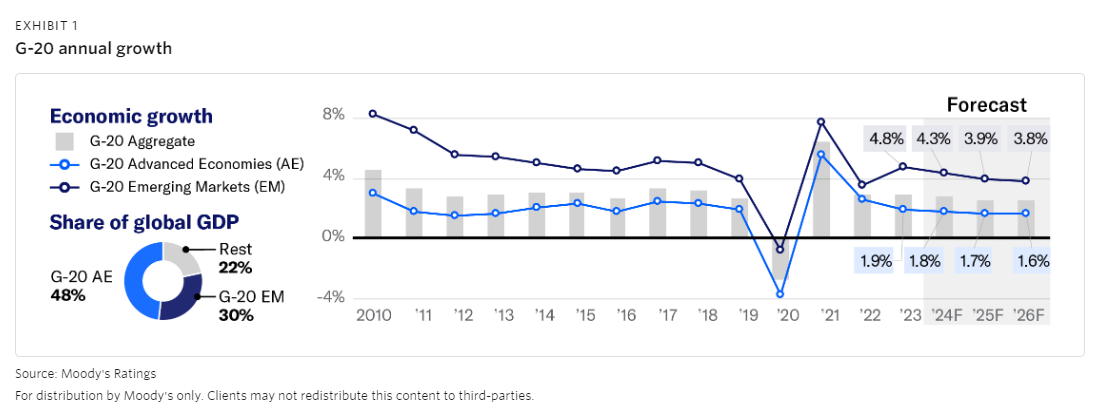

» G-20 economies will post steady but differentiated growth rates. We forecast the G-20 economies will grow by 2.8% in 2024, down from 3.0% in 2023 and moderate through 2026. The US economy is outperforming other advanced economies, though its growth will likely decelerate despite the strong momentum. Europe's sluggish recovery will gradually firm. China 's (A1 negative) growth will likely slow even as stimulus measures are implemented. Rising trade protectionism and a push in several large economies to strengthen domestic industries makes external demand a less reliable source of growth.

» Increased trade tensions and geopolitical stresses are primary risks to the macro outlook. The inclusion of North Korean soldiers by Russia in Ukraine (Ca stable), rising tensions in the South China Sea and the Taiwan Strait and expanding conflicts in the Middle East contribute to a tense international backdrop. Competition between the US and China will shape policies, potentially raise global trade barriers and trigger trade or currency wars. This long-term geoeconomic fragmentation could further split the global economy into geopolitical blocs, complicating global trade and financial connectedness, further dampening global growth.

» Reductions in global policy interest rates will end in 2025. We expect core inflation will decline to near central bank targets by mid-2025, facilitating movement of policy rates toward neutral stances. Synchronized easing will help bolster economic stability but at least some of this may be countered by heightened risks to US inflation from policies proposed by the incoming administration of Donald Trump. We expect the Fed will adopt a cautious approach to policy normalization.

» Change in US administration injects greater policy induced uncertainty. The new US administration will inherit an economy with surprising strength but for forecasting purposes we assume that the net effect of policies will exert a small drag on economic activity. Other than that, we do not account for changes to fiscal, immigration or trade policies until they are implemented.

CREDIT CONDITIONS - GLOBAL