Executive Summary

Leveraged buyout (LBO) competition between broadly syndicated and direct lenders will continue, as interest rates ease, defaults fall, and refinancing for collateralized loan obligations persist.

Read our 2025 outlooks for Global leveraged finance and Global CLOs:

» Global leveraged finance: Improving credit conditions will boost deal flow, but risks to persist

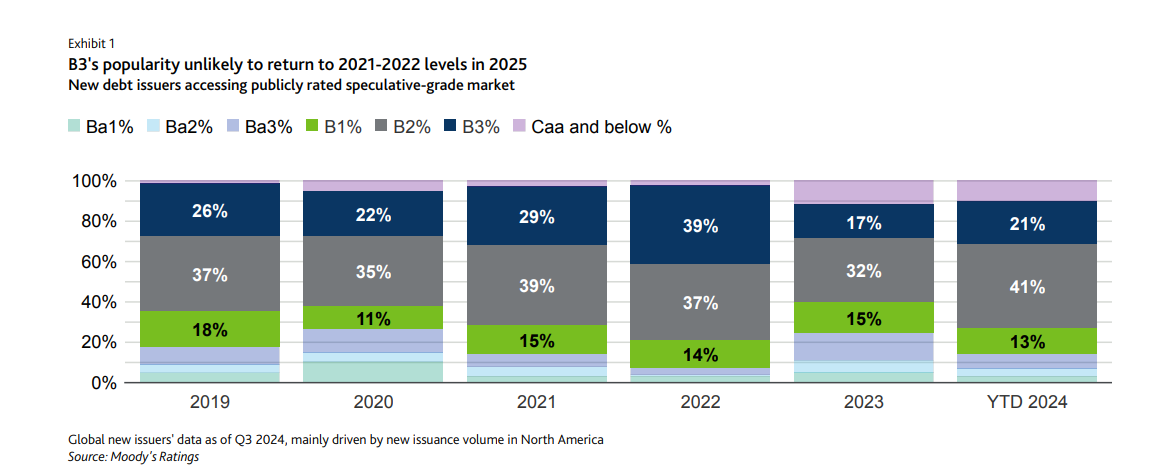

As interest rates decline, credit fundamentals will improve in 2025 and defaults will ease. Investors will hunt for yield and private equity funds will need to deploy some $9 trillion of global dry powder, boosting market liquidity and deal flow. Deal activity will be concentrated in North America and EMEA, where leveraged finance markets remain larger and demand stronger. Leveraged buyout (LBO) activity is gathering pace after a slow start to 2024, although much less so in APAC and LatAm. Investors will remain focused on higher-quality borrowers, while private equity sponsors will focus on financial flexibility and returns.

Borrower-friendly market conditions will spur greater deal activity. LBO deal momentum will be better supported in 2025 as borrowers gain more confidence that interest rates are easing and as valuations improve. We expect more flexible credit protections as deal competition persists between direct and broadly syndicated loan (BSL) lenders. Leveraged loan issuers will also continue to pursue opportunistic repricings and refinancings, which dominated deal activity in 2024.

» Global CLOs: Strong economy, low rates will bolster performance and refi volume

Continued growth and declining interest rates will aid corporate borrowers in both the US and Europe, leading collateralized loan obligation (CLO) collateral defaults to decline. Speculative-grade defaults will decline over the course of 2025 to reach 2.6% and 2.7% in October in the US and Europe, respectively, down from 5.6% and 3.3% in October 2024. As competition between broadly syndicated lenders and direct lenders (private credit) intensifies, covenant flexibility and other characteristics typical of broadly syndicated loans (BSLs) will increasingly migrate to private credit. Expiring non-call periods in outstanding transactions will provide a continued pipeline of refi issuance if CLO spreads remain low. Middle market CLOs will remain a major component of new US CLO issuance, while CLOs backed by debt from direct lenders will remain a niche product in Europe.

LEVERAGED FINANCE AND CLOs - GLOBAL