As the financial industry continues to experience the transformative effects of artificial intelligence (AI) and Augmented Intelligence on its risk management frameworks, there is no better time to review and anticipate AI, whether it involves machine learning (ML), deep learning (DL), or Generative AI (GenAI).

AI technologies can help Compliance teams perform tasks requiring human intelligence across numerous processes. These technologies can continuously enhance and augment the accuracy and speed of human-led decision-making.

Compliance tools powered by AI technologies can support key processes across the customer lifecycle, including:

They can also contribute to prevention and detection capabilities while maximizing the use of data available to Financial Institutions (FI).

This article draws from a series of exchanges between Olivier Morlet, a money laundering reporting officer (MLRO) and member of the Global Coalition to Fight Financial Crime (GCFFC), and Moody’s Industry Practice Lead, Francis Marinier.

They review six impacts of AI on two key areas - regulatory compliance – specifically around UBO discovery - and social responsibility:

AI algorithms can analyze vast amounts of complex ownership data to identify and understand connections and form patterns. Natural language processing also enables relevant information to be processed and extracted from large volumes of unstructured text in seconds. When applied to beneficial ownership, this can help indicate hidden ownership structures. This allows reporting officers to uncover deliberately tenuous or obscured connections between entities and individuals that would be difficult to detect through human analysis alone.

The changes introduced by the latest generation AI/ML can transform financial crime, possibly leading to faster standardization of use cases, such as customer screening.

The development of unsupervised-training-based programs, which include algorithms and neural networks of parameters, is increasingly being applied in the industry for tasks such as detection, scoring, and investigation.

Early AI methodologies built on supervised model training were often used alongside traditional rule-based systems. However, there is a growing shift towards using unsupervised models to identify patterns, similarities, and/or anomalies within groups of aggregated data while helping to reduce false positives and optimize overall efficiency.

In Moody’s recent study into Entity Verification, 46% of respondents identify improving data quality and accuracy as a key challenge in the field AI-enabled solutions can automate searching for and identifying beneficial owners from multiple data sources. Machine learning models can be trained to recognize indicators of beneficial ownership in corporate filings, shareholder documents, and other records. They can also help calculate ownership percentages within connected, circular ownership structures.

AI can extract data from relevant corporate registries, standardize it, and utilize entity resolution techniques to determine when different records refer to the same entity, facilitating entity consolidation. It can streamline data collection and integrate information to generate comprehensive ownership structure maps, establishing connections between entities, such as shared addresses, directorships, and other factors.

AI can significantly enhance transparency concerning beneficial ownership when worldwide BO registers lack consistency in completeness, format, and accessibility. Harnessing AI alongside a commitment to data completeness and accuracy is quickly emerging as a powerful tool for transparency to assist all who are in the fight against financial crime.

AI-powered social network analysis (SNA) examines the relationships between entities and individuals to uncover potential beneficial ownership connections among many other links between subjects of interest. This approach helps visualize complex ownership structures, identify central nodes that may represent actual beneficial owners, and develop robust, extended network investigations. Since the early 2010s, these extensive network investigations have increasingly utilized the ‘follow the money’ principle to trace financial connections.

Today, SNA can support the identification of Ultimate Beneficial Owners (UBOs) in the following 5 ways:

1. Mapping complex ownership structures

SNA allows for the visualization and analysis of complex ownership networks. By representing entities as nodes and ownership relationships as edges, SNA can map intricate corporate structures and reveal:

This visual representation can make tracking ownership chains to UBOs more efficient.

2. Identifying key players and influencers

SNA techniques, like centrality analysis, can highlight the most influential and connected entities within an ownership network. This can reveal:

These central nodes are often good candidates for UBOs, or entities closely linked to UBOs.

3. Detecting suspicious patterns

By analyzing the structure and characteristics of ownership networks, SNA can flag potentially suspicious patterns that may indicate attempts to obscure beneficial ownership, such as:

4. Supporting risk assessment

SNA metrics can be used to quantify risk factors related to beneficial ownership, for example:

This data can feed into risk-scoring models to prioritize further investigation or enhanced due diligence.

5. Enhancing due diligence

The network perspective provided by SNA can guide and focus due diligence efforts. It allows investigators to:

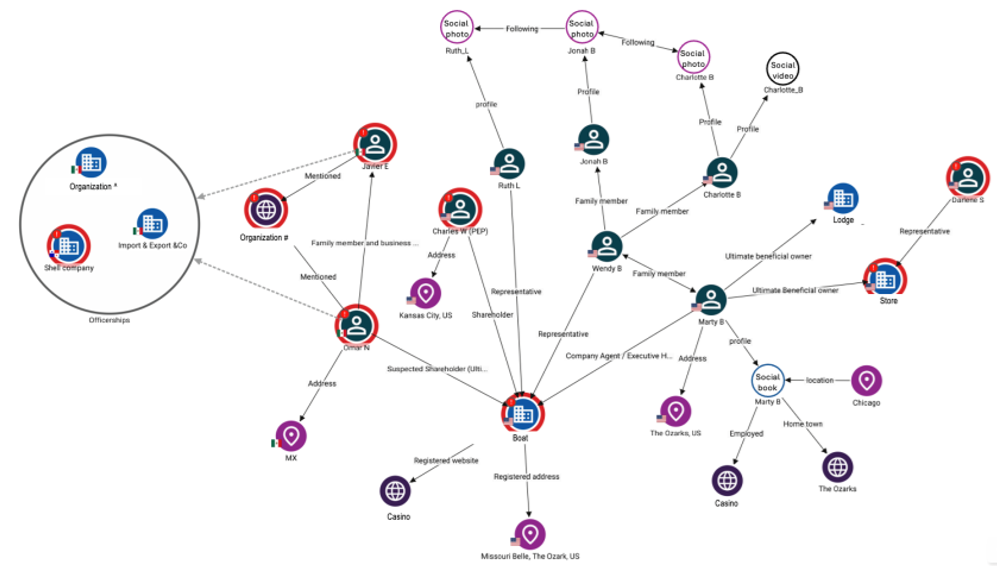

By leveraging SNA techniques and visualization, such as Maxsight™ Investigations, parties engaged in the fight against financial crime can more effectively reveal complex ownership structures, identify UBOs, and detect potential interweaved criminal methodologies to circumvent sanctions, evade tax, defraud through shell companies or layer proceeds of crime. This support reinforces extensive network investigation and provides an opportunity to engage and report nexuses.

Moody’s has significantly invested in supporting organizations utilizing network visualization with models that detect risk in entire company structures based on a global ownership database. Here is a visual representation of an anonymized investigation, encompassing UK, US SDN, and EU sanctions regime breaches, the use of shell companies, and laundering the proceeds of crime.

Many beneficial ownership records exist as unstructured data, such as PDF documents. AI techniques like optical character recognition (OCR) and natural language processing (NLP) can convert these into structured, searchable data. This makes it easier to trace ownership chains.

Data quality is crucial for the success of AI/ML projects. It affects accuracy, reliability, and effectiveness of training models and programs. Improving data processes and integrating external data sources are crucial for enhancing the quality and effectiveness of AI-enabled tools.

This capability is key to areas like making cross-border payments faster, cheaper, more transparent, and more inclusive while maintaining their safety and security in the future.

A key illustration of this benefit is using hybrid data (structured and unstructured) in screening address fields. The Payments Market Practice Group (PMPG) proposed this change in 2024 as part of the FATF Recommendation 16 consultation. Swift and leading Payment Market Infrastructures (PMIs) accepted it for implementation from November 2025 onwards.

Enhancing the fight against the full range of predicate offenses, such as corruption and tax evasion, human trafficking, or terrorism financing, and integrating new ones, such as failing to prevent fraud or sanctions circumvention, requires technology and data-led solutions beyond traditional methods.

The transformative potential of AI/ML compliance tools is an ongoing conversation between regulators and institutions to set the AI/ML scene in ethical, technical, and practical terms. This is the Public Private Partnership approach.

The crux is for financial institutions to begin transforming AI/ML compliance journeys under the encouragement and supervision of regulators to ensure the safe deployment of new technologies.

This also creates a growing need for compliance officers versed in regulatory frameworks who are innovative, data-driven, and AI/ML savvy. These skills are essential in navigating the nuanced challenges of modern financial institutions, which need to be armed with a solid risk-based approach. Their expertise can help foster an environment where compliance is more than a regulatory requirement; it becomes a dynamic component of strategic decision-making.

Bias in AI can originate from different sources, including but not limited to:

If not carefully curated, training data can carry historical biases or reflect societal inequalities that AI models inadvertently learn and perpetuate. More broadly, AI/ML tools can only process data they have been exercised to detect, recognize, and analyze.

Adopting transparent AI/ML methodologies that allow for examining and understanding how “alerts” are generated can help facilitate trust among users and stakeholders. From this point of view, supervised training models that depend on historical decisions and a “known/tested” dependency between input received and desired output may pose a different risk compared to semi-supervised and unsupervised training models that depend on patterns and search for similarities, as highlighted by Chelsea Carrick & Fred Williams in a recent reflection on historical bias in AI-based AML systems for ACAMS1.

AI and ML are redefining compliance in the financial services sector. They offer sophisticated tools to increase corporate transparency and detect and prevent financial crimes more effectively. Despite challenges with complexity, data, and historical bias, the potential benefits for regulatory compliance and societal well-being are immense.

As the industry navigates these technologies, collaboration between actors, innovators, and regulators is essential to establish ethical principles and realize the technologies’ full potential.

Moody’s is helping to transform compliance and third-party risk management. Integrating award-winning data, workflow automation, and AI-driven solutions creates a world where risk is understood so decisions can be made with confidence, including with the support of Maxsight™ Investigations.

Please get in touch with us if you would like more information about our compliance solutions. We would love to hear from you.

1 https://www.moneylaundering.com/news/historical-bias-could-undermine-artificial-intelligence-based-aml-systems/?