Financial scams orchestrated by complex organized crime networks are reaching alarming levels, in part accelerated by the increasing use of artificial intelligence and cryptocurrency. According to a 2024 report by the Global Coalition to Fight Financial Crime, the estimated proceeds from scam losses across Australia, Hong Kong, Singapore, United Kingdom, Canada, and the United States amount to $114 billion – comparable with the GDP equivalent of the 64th largest country.

In this fireside chat, Linshan Tiong, Associate Director of Marketing for Asia-Pacific and the Middle East, sat down with Choon Hong Chua, Head of Financial Crime Practice Group for Asia-Pacific and the Middle East, to discuss some burning questions on financial crimes today, including:

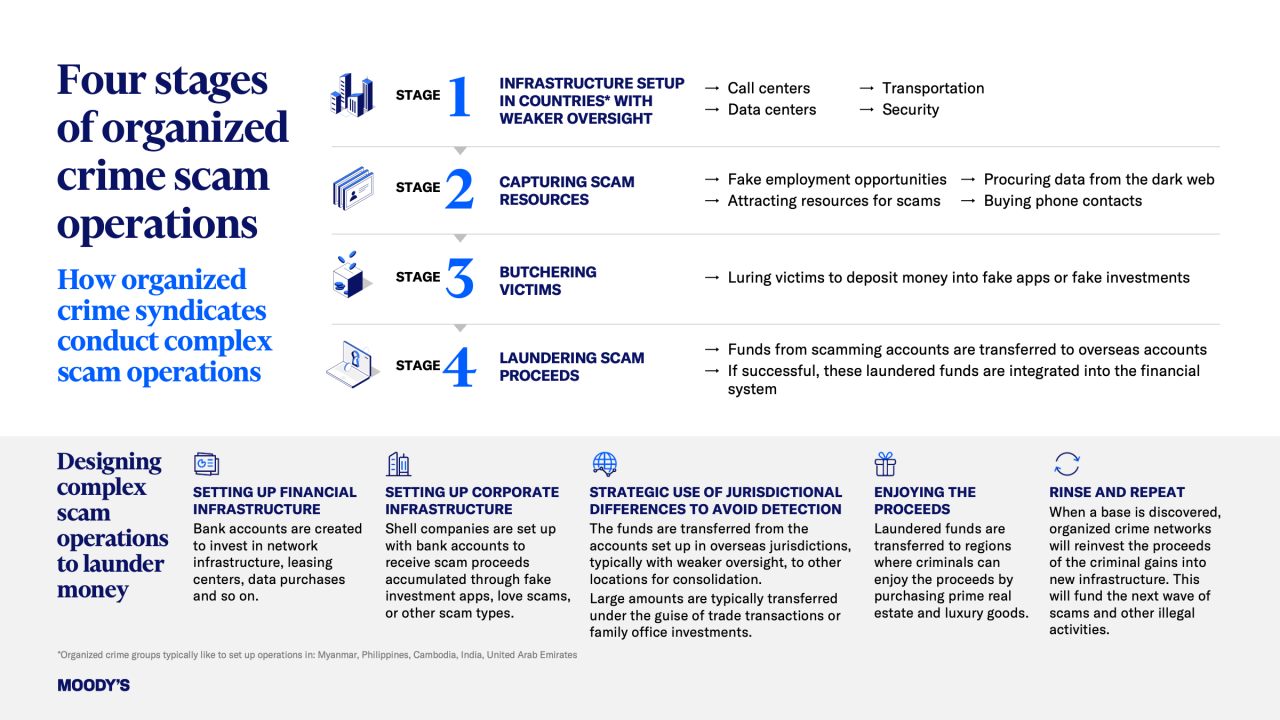

The emergence of complex, technology-enabled scams run on a massive scale poses huge risks to consumers and banks. In Southeast Asia, factors such as improved digital connectivity, fragmented regulations, civil conflict, and corruption have contributed to the problem. These factors, fueled by criminals’ use of advanced, methodical ways to operate scams, create an environment for syndicates to generate and launder illicit proceeds.

Our financial crime experts observe that organized crime networks strategically establish themselves in countries where they can take advantage of civil conflict or instability. They set up legitimate physical and technical infrastructure – call centers or scam centers – to lure victims into forced labor conditions. Once ensnared, victims are coerced into conducting scams, with the proceeds then integrated into the financial system. This cycle perpetuates as illicit gains are reinvested into building new scam operations.

As scammers refine their tactics to exploit vulnerabilities, new scam typologies – from digital currencies, to telecommunications, to investment frauds – are on the rise. INTERPOL’s 2024 Global Financial Fraud Assessment highlighted the increase in digital scams and human trafficking fraud globally, with Asia being particularly vulnerable to “pig butchering” scams.

As scams can be notoriously difficult to trace, financial institutions play an important role as intermediaries between scam operations and the laundering of proceeds. This is where banks can dig deeper, beefing up their compliance and third-party risk controls.

While the easiest way to detect red flags would be to run entities or individuals against official lists, some criminal networks or associated individuals with no prior enforcement actions taken against them would not be on these lists. In this case, financial institutions can look out for other indicators that signal suspicious activity: multiple concurrent directorships, nominee arrangements, or weak indications of actual operations could suggest shell companies are potentially being used to launder scam proceeds.

Beyond traditional customer due diligence procedures, financial institutions can also leverage advanced analytics and automation tools to streamline compliance processes and improve efficiency. Automated know your customer (KYC) checks and intelligent screening solutions alert companies to changes in counterparty networks, helping them to mitigate potential issues early. The ability to see hidden risks in their network – by unraveling complex ownership structures or revealing ultimate beneficial ownership – also help organizations manage and address growing risk promptly.

An always-on approach, otherwise known as perpetual KYC (pKYC), also helps organizations strengthen their detection and prevention efforts using real-time, event-based triggers to update changes in a customer’s profile. This can be incorporated within our client lifecycle solution that enables companies to tailor triggers to their risk policies and create automated workflows. By reducing the need for manual, periodic reviews, pKYC empowers compliance teams to react to real-time changes in the risk profiles in their network.

Given the rise of scam attempts throughout the world, one may wonder why and where detection is falling short. It is important to consider certain operational complexities at play, such as an inevitable delay between banks reporting suspicious activity and authorities gathering additional intelligence.

As criminal masterminds operate in a wider financial ecosystem, aligning multi-sector priorities and efforts for a more effective response can be useful. Organizations should continue banding together to fight financial crime.

Recent achievements in the region demonstrate the power of collaboration. Hong Kong’s Fraud and Money Laundering Intelligence Taskforce (FMLIT), an intelligence-sharing platform used by the national police, regulator, and several banks, is a case study on the efficacy of public-private cooperation. Since the creation of FMLIT in 2017 till October 2023, approximately HK$1.1 billion in crime proceeds has been restrained or confiscated.

Financial institutions are also increasingly adopting a risk-based approach in the fight against scams. Unlike rigid rules that rely on preset thresholds and criteria, a risk-based approach allows institutions to tailor their detection strategies based on the specific risks posed by different customers and transactions.

For example, sudden, large transactions to unfamiliar overseas accounts may trigger alerts under a risk-based approach in the context of several factors: customer's profile; transaction history; or regulatory environment of the destination country. When institutions customize triggers based on their risk appetite and business objectives, compliance teams can prioritize resources and focus due diligence efforts on higher-risk activities and customers.

As scams persist, financial institutions are tasked with proactive responses and prevention at the root of the crime, not just detecting it when illicit proceeds have been flagged in the system. It will take a multi-sector approach to outsmart financial criminals and preserve trust in the global financial system.

Organized crime groups will continue innovating new ways to outsmart the financial system. However, more collaboration, stronger compliance controls, and the right tools can all aid in financial crime detection and prevention.

To find out more about how Moody’s can help your organization uncover hidden risk, get in touch today.