In banking, understanding risk has most often started with knowing the customer. But as corporate structures become more complex and financial crime methods evolve, that principle may extend beyond individuals to the businesses they represent.

This is where Know Your Business (KYB) comes into greater focus. KYB brings a set of core objectives into a corporate context: building a clearer, evidence-based view of who the bank is doing business with, and the risks that may carry.

Know Your Business (KYB) is the process of verifying the identity, ownership, and risk profile of a company before establishing or maintaining a financial relationship.

While KYC focuses on individuals, KYB applies similar principles to legal entities. It involves assessing whether a business exists and operates as expected, and whether it may be used to obscure illicit activity.

At a practical level, KYB can help banks answer 3 questions:

Answering these questions may help form the foundation of corporate onboarding and ongoing due diligence.

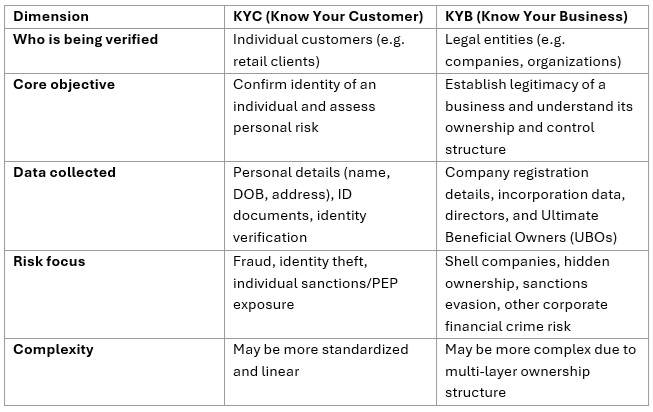

Five differences between KYC and KYB?

KYB is a component of several anti-money laundering (AML) and counter-terrorist financing (CTF) frameworks globally. For compliance with regulatory frameworks such as the US Patriot Act, the UK Money Laundering Regulations 2017, and the EU AMLR, financial institutions are typically required to verify corporate customers before offering services such as account opening, lending, or payments.

The reason is that corporate structures may be used by bad actors to obscure ownership, which can be associated with money laundering, sanctions evasion, fraud, or other types of crime.

Without a clear view into beneficial ownership and business activity, banks may face regulatory scrutiny, financial loss, or reputational damage.

KYB is therefore an important risk management discipline and supports customer-related decision-making across the lifecycle of a relationship.

Although implementation varies, many KYB processes follow a similar structured, risk-based approach.

Despite its structured approach, KYB can be operationally complex.

Many businesses operate across jurisdictions with layered ownership structures that may be difficult to untangle. Accessing consistent, up-to-date information on entities and their owners can be challenging, particularly in markets with limited visibility.

At the same time, banks may have fragmented data sources or manual processes, which may create duplication, delays in onboarding, and challenges in maintaining a consistent view of risk across entities.

Regulatory expectations are also evolving. Institutions may be required to demonstrate visibility into beneficial ownership and maintain current information throughout the customer relationship.

These pressures can make it more difficult to balance thorough due diligence with efficient customer experiences.

As part of a broader evolution in risk management and compliance, KYB is shifting from static checks toward more dynamic approaches.

Traditional models may rely on periodic reviews i.e. revisiting customer information at fixed intervals. However, risk does not change on a fixed schedule. Ownership structures can shift, companies can expand into new markets, and new risk signals may emerge over time.

A more connected approach focuses on identifying trigger events, such as ownership changes, sanctions updates, or adverse media, and responding as they occur. This may require bringing together multiple data points, including entity information, ownership structures, and external risk signals, to develop a more unified view.

At its core, KYB is about developing greater clarity around corporate customers, helping banks build a structured and defensible view of the businesses they engage with, and supporting that understanding over time.

To achieve this, some key questions may include:

Addressing these questions may support compliance and risk-related decision-making.

Moody’s solutions for KYB include entity verification tools, access to beneficial ownership data, screening and due diligence workflows, and capabilities for ongoing monitoring.

Moody’s works with customers to help tailor KYB approaches to their processes, integrating data checks into workflows and using AI-based capabilities to support efficiency and analysis.

For more information, please get in touch with our team.

*Disclaimer: This content is for informational purposes only and does not constitute legal, financial, compliance or other professional advice. Please consult with a qualified professional for specific legal, financial, compliance, or other professional advice. For more terms and conditions pertaining to Moody’s products and services, refer to the https://www.moodys.com/web/en/us/legal/global-disclaimer.html on Moody’s website.